Disclaimer: In this assignment, I have utilised Claude 4 Sonet in various aspects, including clarifying the expectations of the questions, facilitating my understanding of the addressed concepts, roxygen2-style document generation for helper functions, code debugging, and proof-reading.

Exercise 1 - Financial Data#

a. Stylized Facts Analysis#

i. Data Crawling & Prepocessing#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

|

if (!file.exists("Data/price_dt.rds")) {

# Download Data

stock_ls <- c("COST", "WMT", "KO", "PEP")

price_dt <- tq_get(stock_ls,

get = "stock.prices",

from = "2000-01-01",

# to = as.character(Sys.Date() - 1)

to = "2025-08-09"

)

# Save model data

saveRDS(price_dt, file = "Data/price_dt.rds")

} else {

# Access saved stock data

price_dt <- readRDS("Data/price_dt.rds")

}

# Prepare return data

return_all_dt <- prep_return_dt(price_dt)

# Extract different frequencies

daily_returns <- return_all_dt$daily

weekly_returns <- return_all_dt$weekly

monthly_returns <- return_all_dt$monthly

head(daily_returns)

|

1

2

3

4

5

6

7

8

9

|

## # A tibble: 6 × 9

## symbol date adjusted ret grossret logret sqret absret volume

## <chr> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 COST 2000-01-04 28.1 -0.0548 0.945 -0.0563 0.00317 0.0563 5722800

## 2 COST 2000-01-05 28.6 0.0171 1.02 0.0169 0.000287 0.0169 7726400

## 3 COST 2000-01-06 29.2 0.0201 1.02 0.0199 0.000396 0.0199 7221400

## 4 COST 2000-01-07 31.1 0.0662 1.07 0.0641 0.00411 0.0641 5164800

## 5 COST 2000-01-10 31.8 0.0208 1.02 0.0206 0.000425 0.0206 4454000

## 6 COST 2000-01-11 30.6 -0.0355 0.964 -0.0362 0.00131 0.0362 2955000

|

1

2

3

4

|

# Calculate 5% quantile

daily_q5_dt <- quantile(daily_returns |> pull(ret), probs = 0.05)

weekly_q5_dt <- quantile(weekly_returns |> pull(ret), probs = 0.05)

monthly_q5_dt <- quantile(monthly_returns |> pull(ret), probs = 0.05)

|

Compute summary statistics

1

2

3

4

5

6

7

8

9

10

11

12

13

|

summ_stats <- summary_statistics(

daily_returns, weekly_returns, monthly_returns,

ticker_name = "KO"

)

# Transpose result

summ_stats %>%

mutate(Asset_Freq = paste(Asset, Frequency, sep = " ")) %>%

select(-Asset, -Frequency) %>%

column_to_rownames("Asset_Freq") %>%

t() %>%

round(4) %>%

as.data.frame()

|

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

|

## KO Daily KO Weekly KO Monthly

## Observations 25752.0000 5344.0000 1232.0000

## Mean 0.0004 0.0017 0.0074

## Median 0.0005 0.0027 0.0104

## Std_Dev 0.0145 0.0306 0.0552

## Variance 0.0002 0.0009 0.0030

## Minimum -0.2426 -0.3767 -0.5264

## Maximum 0.1398 0.2008 0.2022

## Skewness -0.3658 -0.9914 -1.1111

## Kurtosis 16.4269 13.2266 10.7056

## Excess_Kurtosis 13.4269 10.2266 7.7056

## VaR_5pct -0.0210 -0.0443 -0.0850

## VaR_1pct -0.0399 -0.0861 -0.1521

## Sharpe_Ratio 0.0245 0.0557 0.1342

## JB_Statistic 194016.1081 24162.8317 3301.4637

## JB_PValue 0.0000 0.0000 0.0000

|

iii. Graphical Examination#

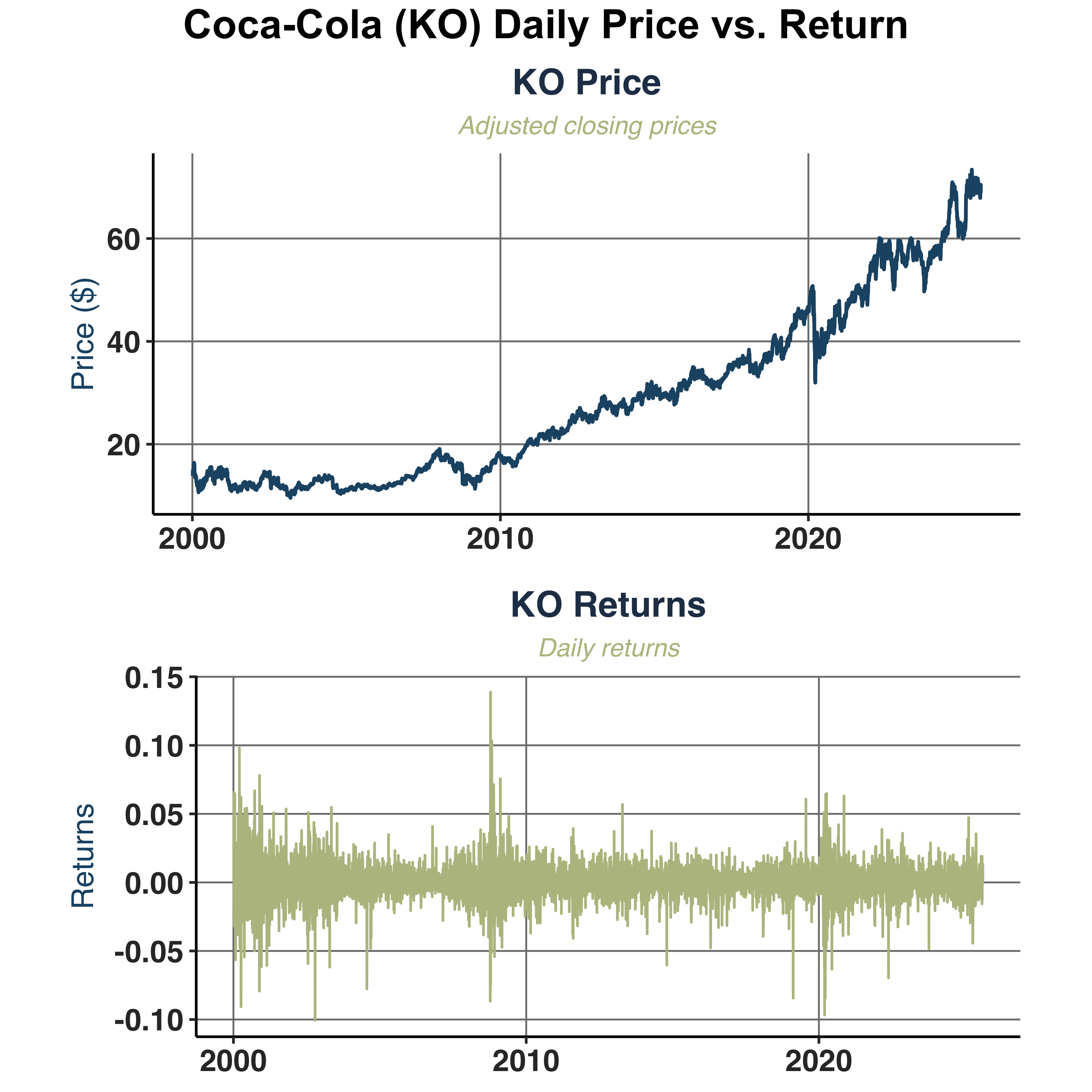

Compare daily adjusted closing prices against daily returns of Coca-Cola (KO).

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

|

# Extract Coca-Cola (KO)

KO_daily <- filter(daily_returns, symbol == "KO")

KO_weekly <- filter(weekly_returns, symbol == "KO")

KO_monthly <- filter(monthly_returns, symbol == "KO")

price_return_plt <- plot_price_return(KO_daily, ticker_name = "KO",

save_pdf = TRUE, filename = "Plots/KO_Price_Return",

plot_width = 6, plot_height = 4)

combined_chart <- price_return_plt$combined

# Add grand title

combined_chart <- annotate_figure(combined_chart,

top = text_grob("Coca-Cola (KO) Daily Price vs. Return",

color = "black",

face = "bold",

size = 16))

combined_chart

|

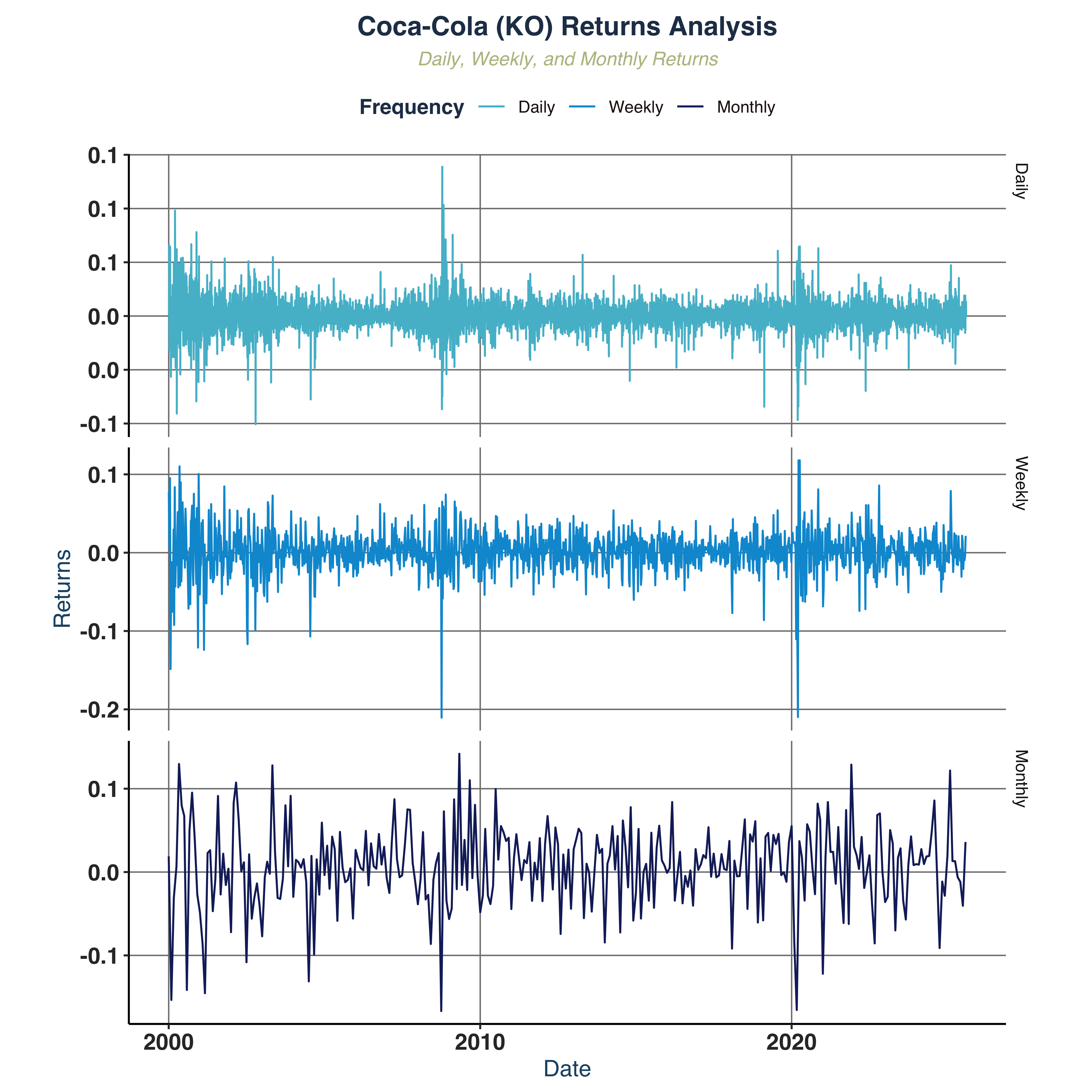

Compare returns across frequencies.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

|

# Combined plotting data

return_plot_dt <- rbind(

select(KO_daily, c("date", "ret")) %>% mutate(freq="Daily"),

select(KO_weekly, c("date", "ret")) %>% mutate(freq="Weekly"),

select(KO_monthly, c("date", "ret")) %>% mutate(freq="Monthly")

) %>%

mutate(freq = factor(freq, levels = c("Daily", "Weekly", "Monthly")))

# Line plot

returns_freq_plt <- return_plot_dt %>%

ggplot(aes(x = date, y = ret, colour = freq)) +

geom_line(size = 0.5) +

scale_color_manual(values = c("Daily" = "#54BCD1FF",

"Weekly" = "#0099D5FF",

"Monthly" = "#172869FF")) +

scale_y_continuous(labels = comma_format(accuracy = 0.1)) +

facet_grid(freq ~ ., scales = "free_y") +

labs(

title = "Coca-Cola (KO) Returns Analysis",

subtitle = "Daily, Weekly, and Monthly Returns",

x = "Date",

y = "Returns",

color = "Frequency"

) +

global_fonts

# Save with appropriate dimensions for vertical layout

ggsave("Plots/KO_Returns_By_Frequencies.pdf", returns_freq_plt,

width = 8, height = 6, dpi = 300)

returns_freq_plt

|

Plot log returns, squared returns, and absolute returns.

1

2

3

4

5

6

7

8

9

10

11

12

|

daily_ret_plot <- plot_return_derivatives(

KO_daily, ticker_name = "KO",

save_pdf = TRUE, filename = "Plots/KO_daily_return_derivatives",

plot_width = 6, plot_height = 3)

daily_ret_combined <- daily_ret_plot$combined

daily_ret_combined <- annotate_figure(daily_ret_combined ,

top = text_grob("Coca-Cola (KO) Daily Returns Comparison",

color = "black",

face = "bold",

size = 16))

daily_ret_combined

|

1

2

3

|

# Note:

# We can apply the same logic and plot for weekly & monthly frequencies but I feel

# it's a bit abundant here. Thus, I only focus on daily basis analysis

|

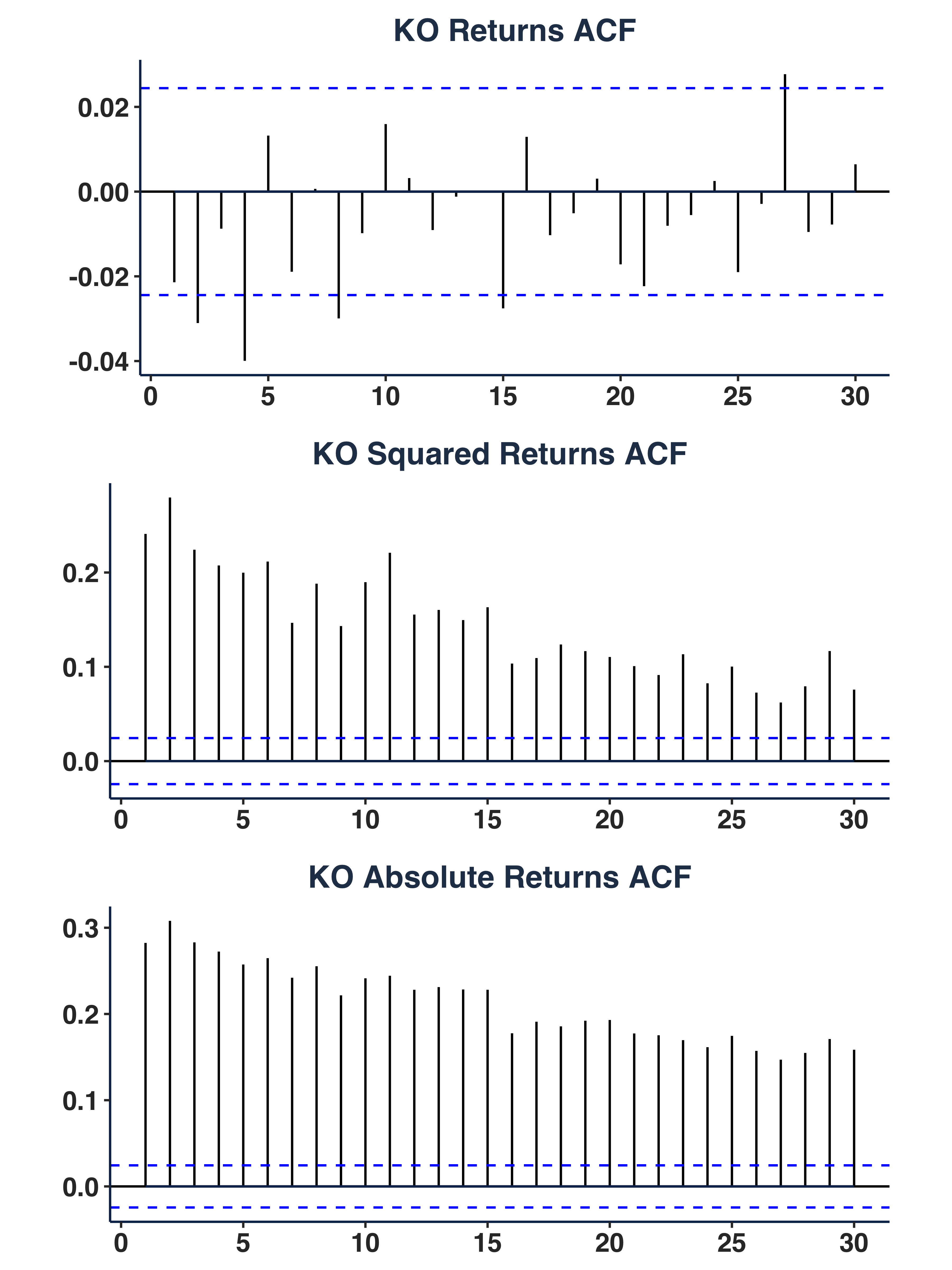

Plot autocorrelation function.

1

2

3

4

5

6

7

8

|

ret_acf_plots <- plot_acf_series(data = KO_daily,

ticker_name = "KO",

lag = 30,

save_pdf = TRUE,

filename = "Plots/ACF_Plots",

plot_width = 6,

plot_height = 3)

ret_acf_plots$combined_plot

|

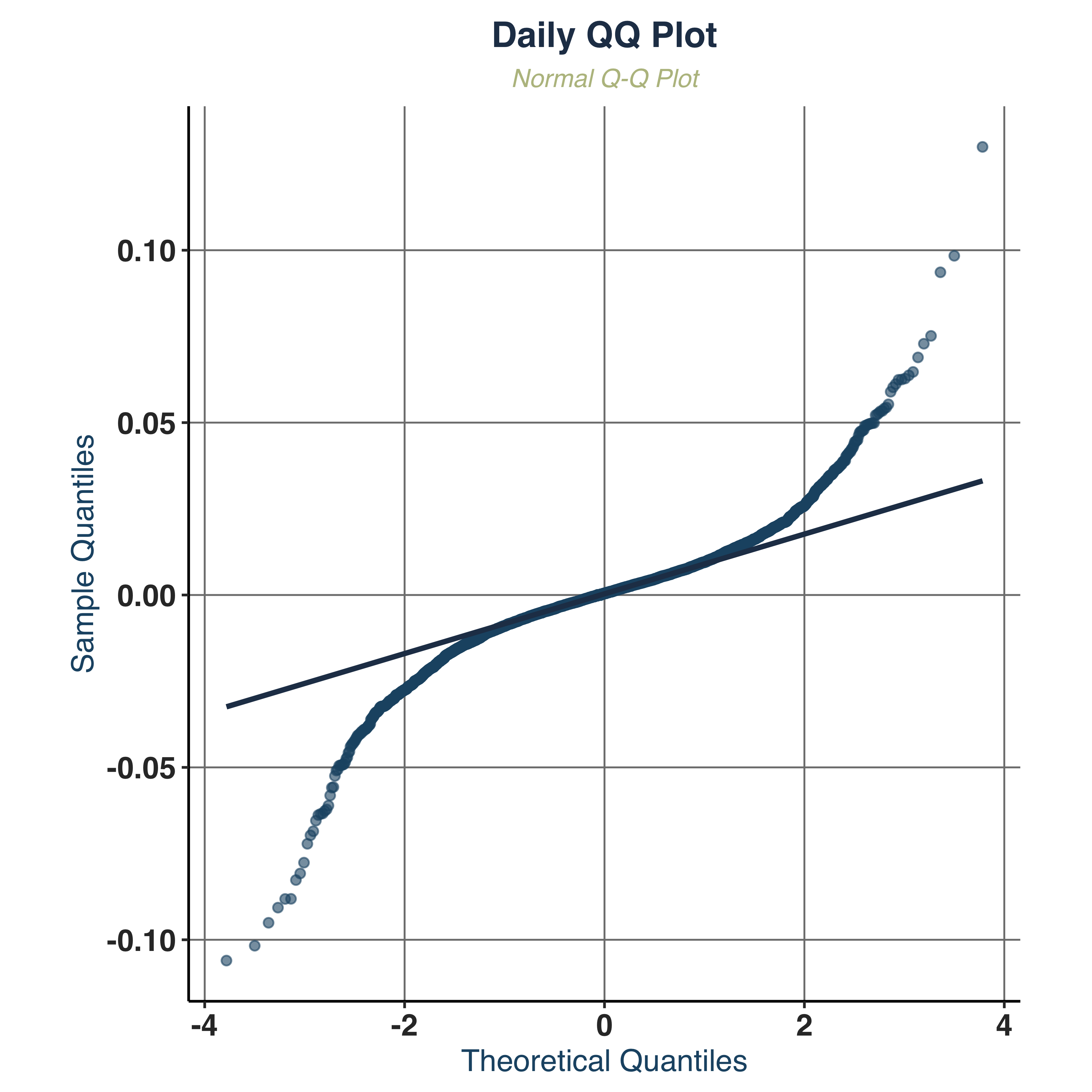

Examine QQ-Plot.

1

2

3

4

5

|

qq_plt <- qq_plot(KO_daily, KO_weekly, KO_monthly,

ticker_name = "KO", save_pdf = TRUE,

filename = "Plots/KO_QQ_Plot",

plot_width = 4, plot_height = 4)

qq_plt$daily

|

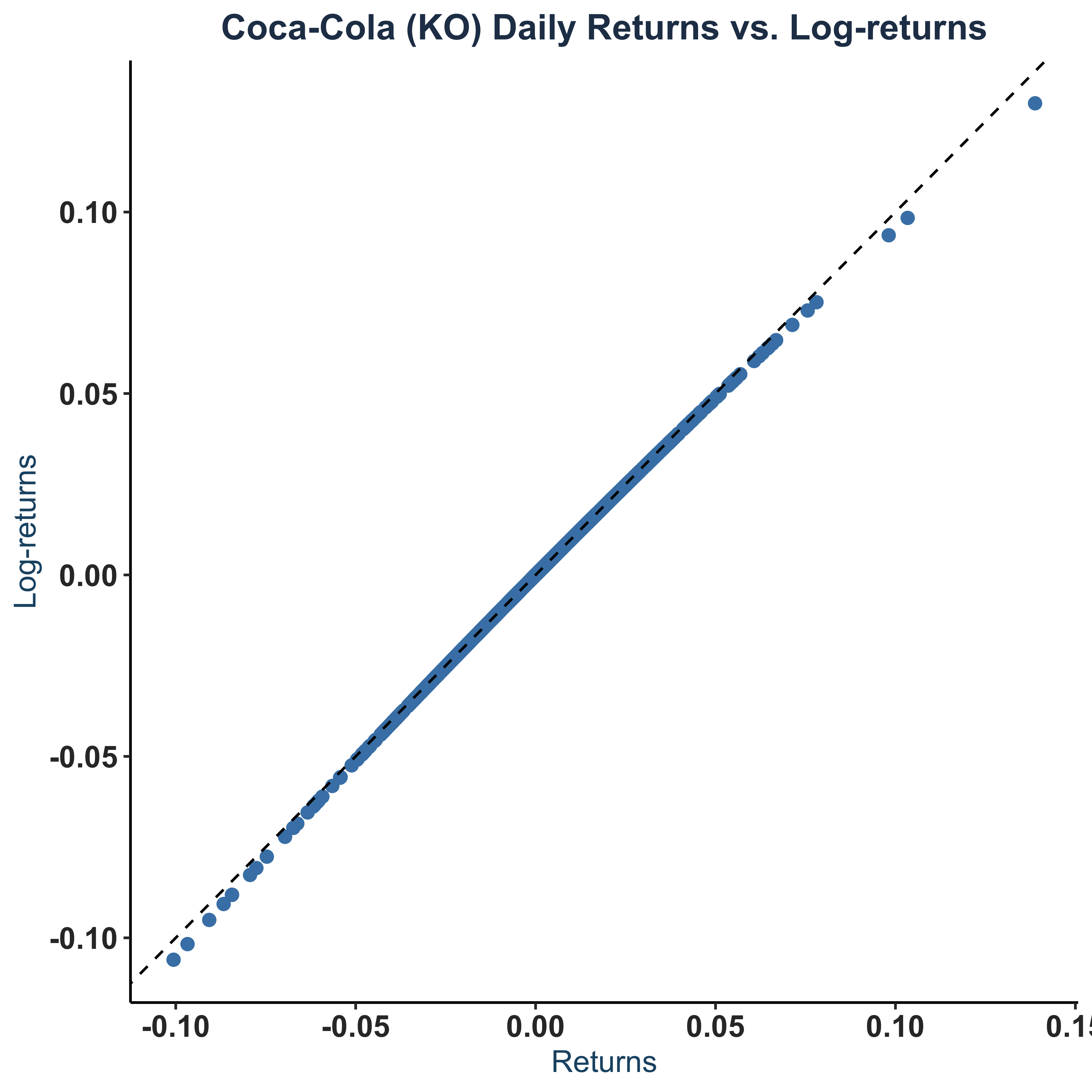

Scatter Plot of returns vs log-returns.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

|

sct_plt <- KO_daily |>

ggplot(aes(x = ret, y = logret)) +

geom_point(color = "steelblue",size=2) +

geom_abline(linetype="dashed") +

theme_bw() +

theme(axis.line = element_line(colour = "black"),

panel.grid.major = element_blank(),

panel.grid.minor = element_blank(),

panel.border = element_blank(),

panel.background = element_blank()) +

labs(

title = "Coca-Cola (KO) Daily Returns vs. Log-returns",

x = "Returns",

y = "Log-returns"

)+

global_fonts

# Save to pdf

pdf(paste0(c("Plots/KO_Returns_LogReturns_Daily.pdf"),collapse = ""),

width=4, height=4)

dev.off()

sct_plt

|

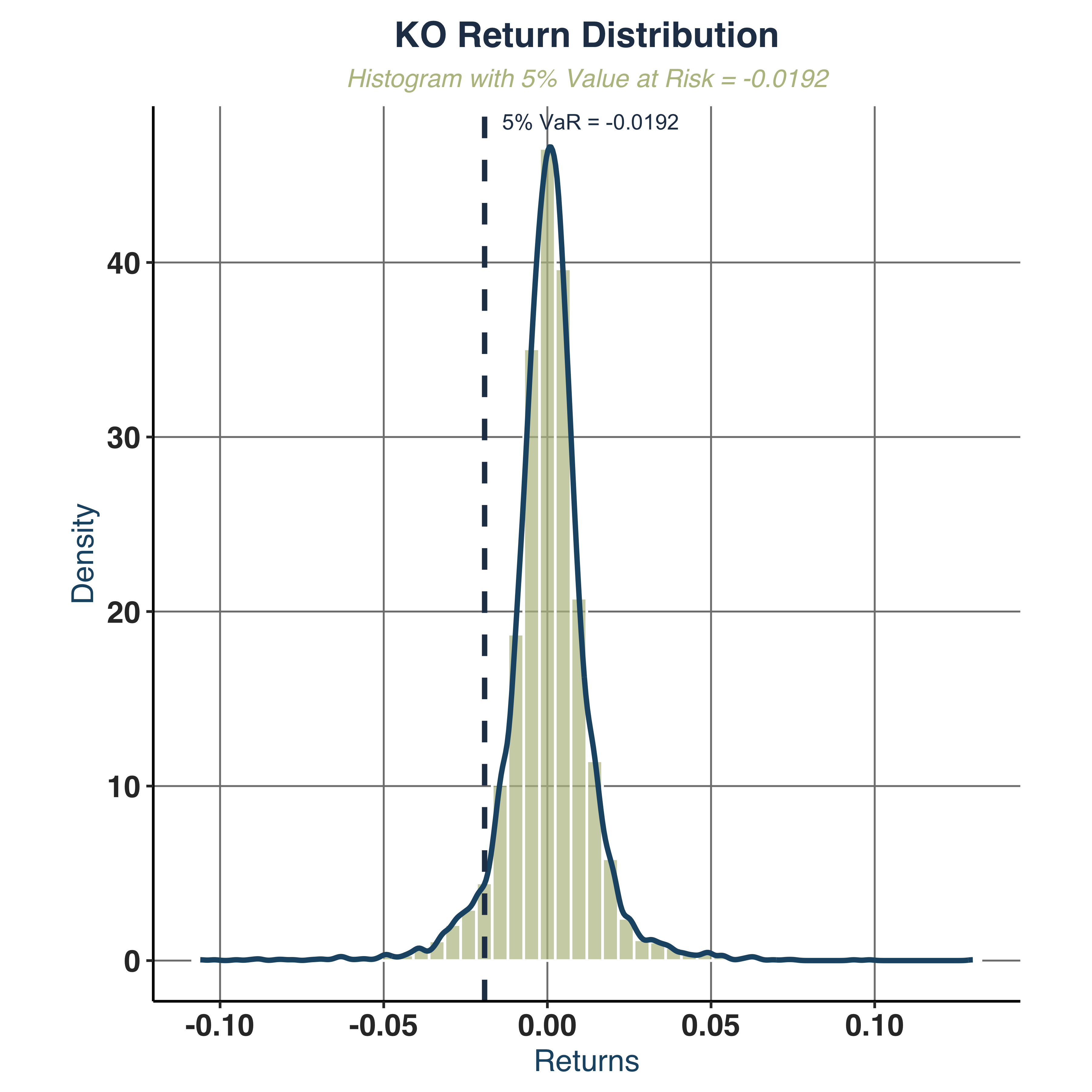

Plot histogram with 5% VaR.

1

2

3

4

|

hist_plt <- plot_histogram_var(KO_daily, ticker_name = "KO",

save_pdf = TRUE, filename = "Plots/KO_Histogram_Analysis",

confidence_level = 0.05)

hist_plt

|

1

2

3

4

|

##

## $var_5pct

## 5%

## -0.01917894

|

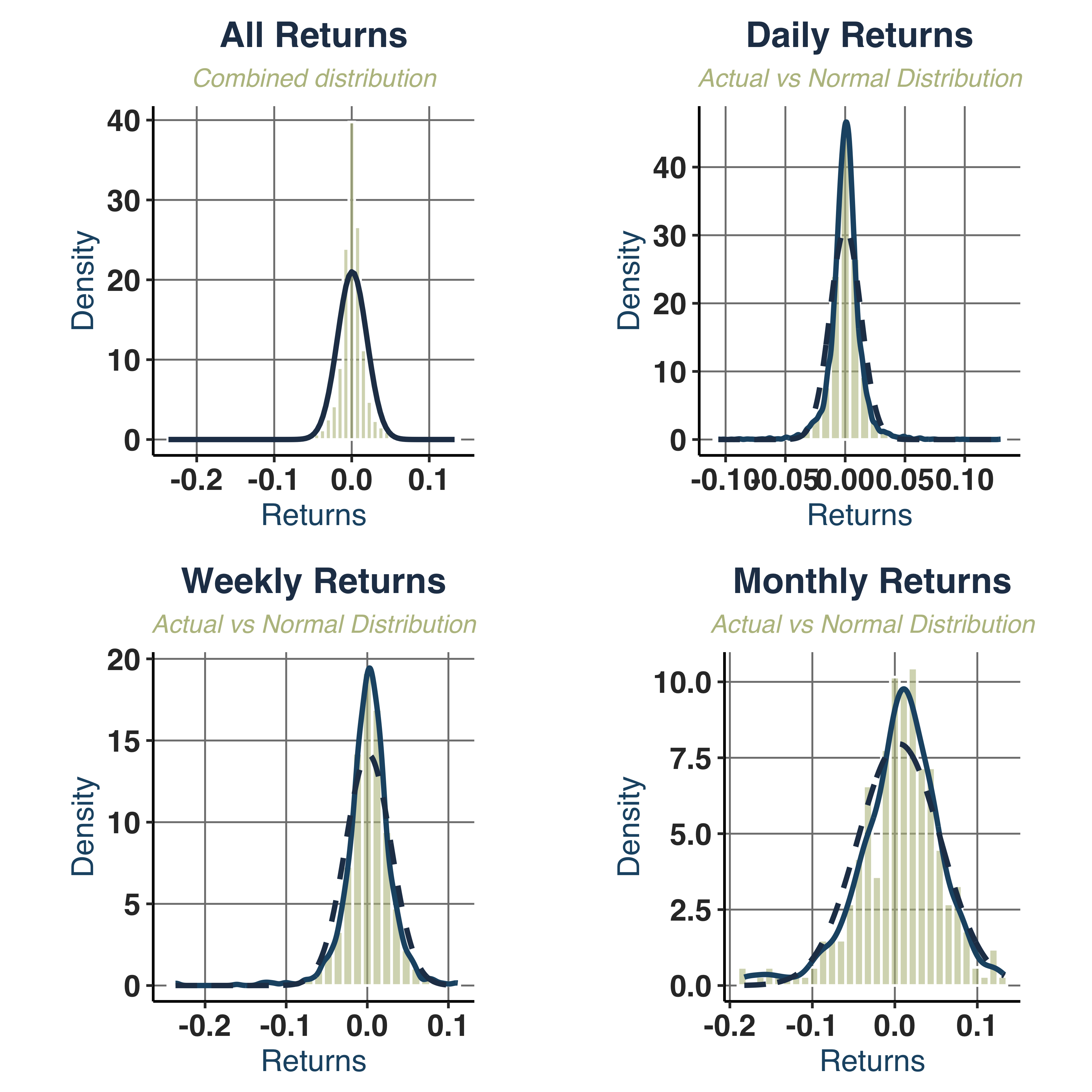

Create a normal distribution with same mean and standard deviation.

1

2

3

4

5

|

norm_dist_plt <- plot_normal_comparison(KO_daily, KO_weekly, KO_monthly,

ticker_name = "KO", save_pdf = TRUE,

filename = "Plots/KO_Normality_Test",

plot_width = 8, plot_height = 6)

print(norm_dist_plt$combined)

|

iii. Analysis of GARCH Properties#

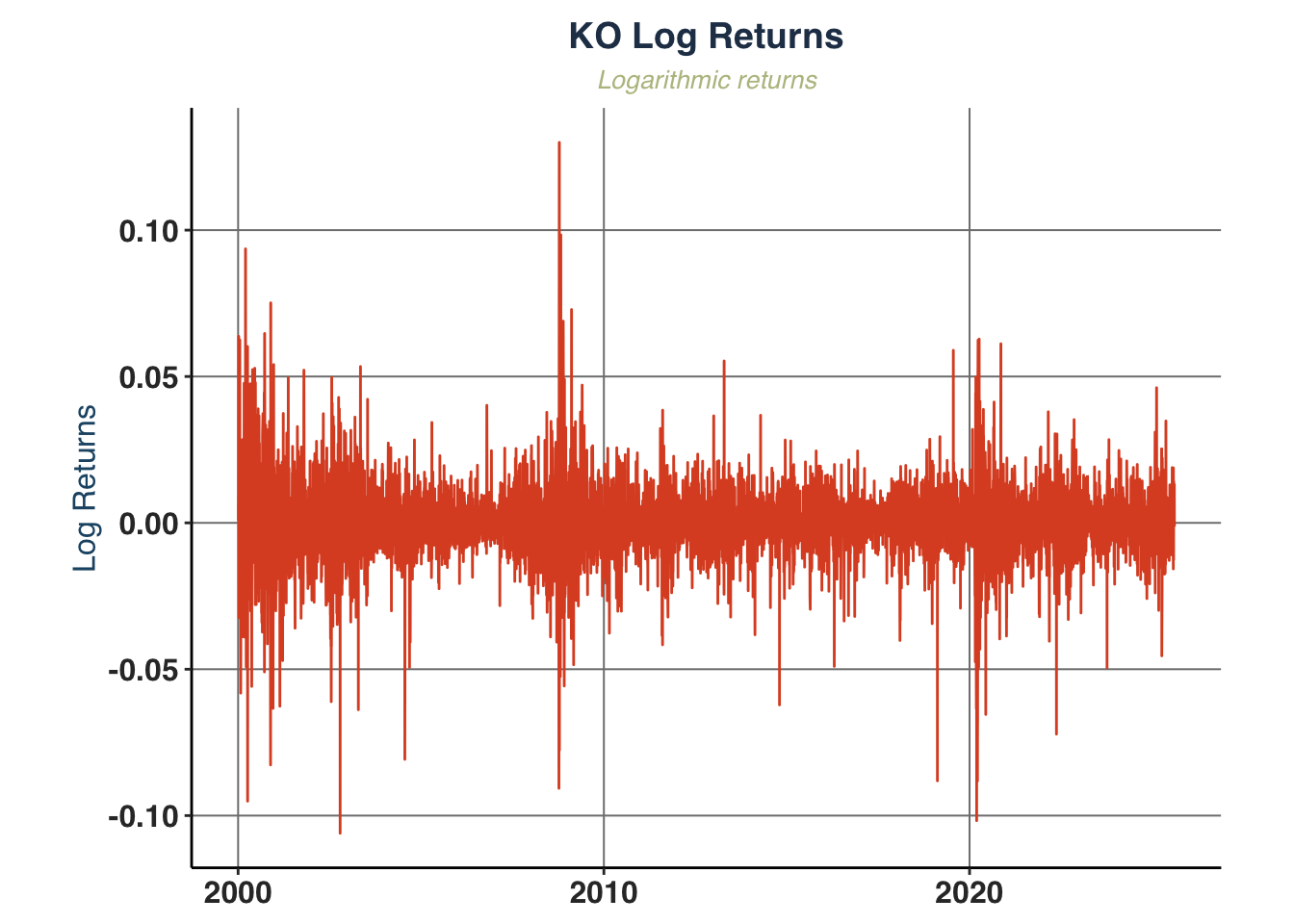

1. Return Distribution:

- Mean Reversion: returns fluctuate around zero mean (

mean=0.0004).

- Negative Skewness (

-0.37): left tail is heavier -> more extreme negative returns.

- Kurtosis (

16.43): fat tail, higher than normal from 7.7 to 13.4.

- Normality:

JB_PValue=0.0000 => strongly rejects normality across all frequencies.

2. Volatility Patterns:

- Volatility Clustering: visible in the returns series, showed in

Coca−Cola (KO) Daily Price vs. Return graph.

- Scale effect: higher frequencies magnify the volatility clustering effect, indicated in

Coca−Cola (KO) Returns Analysis graph.

3. Autocorrelation Structure:

- Returns ACF: fluctuate around `[-0.02, 0.02] -> no linear dependence.

- Squared/Absolute Returns ACF: significant autocorrelation (up to lag 30) -> GARCH effect.

4. Risk Characteristics:

- Value at Risk (VaR):

VaR_5pct range from -2.1% to -8.5%.

- Asymmetric Risk: more downside risks than upside potentials.

- Sharpe Ratio: poorly risk-adjusted performance (

Sharpe_Ratio<0.5 across all frequencies), but it is improved along with holding period.

b. Estimate Conditional Volatility Models#

i. Identify Model Specification#

First, we need to set up lower & upper bound for the model and test for ARCH effect on the squared (log-)returns.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

|

## 1. Setup Estimation Specs ----

# extract interested stock

# Extract log returns for KO

log_ret_real <- KO_daily$logret

ensembles <- 1

y <- matrix(log_ret_real, ncol = ensembles)

# Positivity of parameters and stationarity

lb.GARCH <- c(0.00000001, 0.00000001, 0, 0.00000001)

ub.GARCH <- c(0.2, 0.4, 0.9999, 0.9999)

# starting values: mu, omega, alpha, beta (not used directly in multi-start)

# b0 <- c(0, 0.0001, 0.2, 0.04)

## 2. Test for Model Specs

# i. Ljung-Box test on squared returns

Box.test(y^2, lag = 10, type = "Ljung-Box")

|

1

2

3

4

5

|

##

## Box-Ljung test

##

## data: y^2

## X-squared = 2755.8, df = 10, p-value < 2.2e-16

|

1

2

|

# ii. ARCH test

ArchTest(y^2, lags = 5)

|

1

2

3

4

5

|

##

## ARCH LM-test; Null hypothesis: no ARCH effects

##

## data: y^2

## Chi-squared = 225.68, df = 5, p-value < 2.2e-16

|

1

2

3

4

5

6

7

|

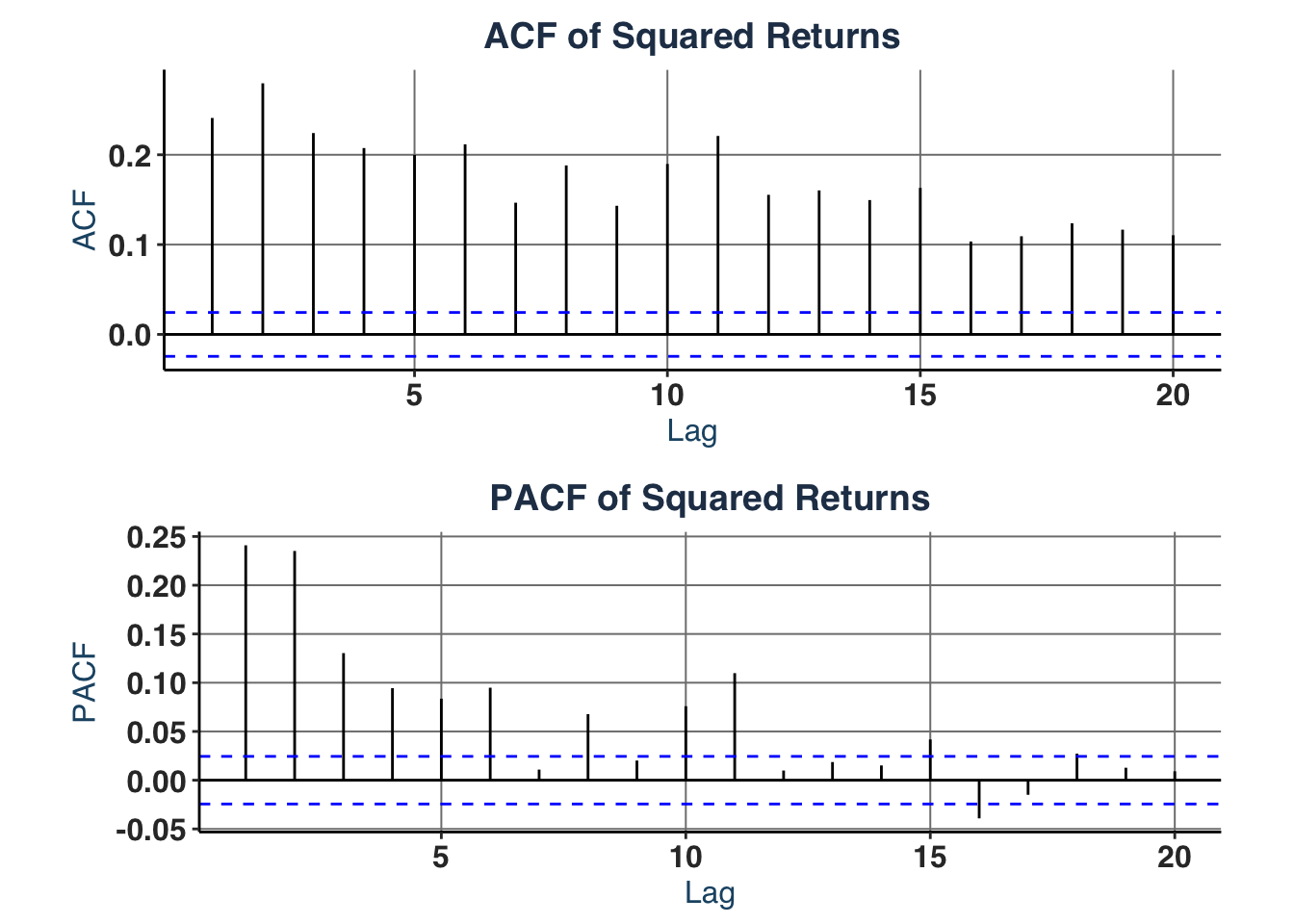

# iii. Partial- & Autocorrelation in squared returns (suggests GARCH order)

acf_plt <- ggAcf(y^2, lag.max = 20) +

labs(title = "ACF of Squared Returns")

pacf_plt <- ggPacf(y^2, lag.max = 20) +

labs(title = "PACF of Squared Returns")

acfs_plt <- ggarrange(acf_plt, pacf_plt, nrow = 2)

acfs_plt

|

1

2

|

# iv. Basic statistics

cat("Skewness:", moments::skewness(y^2), "\n")

|

1

|

cat("Kurtosis:", moments::kurtosis(y^2), "\n")

|

It shows that GARCH(1,1) (base model), GARCH(2,1), or GARCH(3,1) specifications are suitable for the estimate as:

- ACF shows slow, gradual decay -> GARCH term order 1 ($q = 1$).

- PACF shows sharp cutoff after lag 2, but lag 3 is still significant -> ARCH term order 1-3 ($p \in [1,3]$).

We can use GARCH(1,1) model as benchmark for Likelihood Ratio test, even for comparison with other extensions (e.g. GJR-GARCH).

Now, we estimate the base model sGARCH(1,1):

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

|

## 3. Estimate GARCH (Multi-Start) ----

control.solnp <- list( rho = 1,

# penalty weighting scalar for infeasibility in the

# augmented objective function: default is 1

outer.iter = 600,

# Maximum number of major (outer) iterations (default 400).

inner.iter = 800,

# Maximum number of minor (inner) iterations (default 800).

delta = 1e-7,

# Relative step size in forward difference evaluation (default 1.0e-7).

tol = 1e-6)

set.seed(1340) # for reproducibility

if (!file.exists("Data/KO_GARCH_base_mdl.rds")) {

base_mdl <- estimate_garch_dynamic(

y = y,

n_starts = 10, # change number of random starts here, better set to 100

garch_order = c(1,1),

model_type = "sGARCH", # choose model

distribution = "norm", # choose error distribution

lower_bounds = lb.GARCH,

upper_bounds = ub.GARCH,

loglik_func = Likelihood.GARCH,

ineq_constraints = Inequality.constraints.GARCH,

custom_control = control.solnp

)

# Save results

saveRDS(base_mdl, file = "Data/KO_GARCH_base_mdl.rds")

} else {

# Access saved data

base_mdl <- readRDS("Data/KO_GARCH_base_mdl.rds")

}

|

1

2

3

4

|

## 4. Display Result ----

# Print best SOLNP results

stock_name <- "KO"

head(base_mdl$best_estimates$solnp, -1)

|

1

2

|

## mu omega alpha beta

## -2.315184e-06 8.401866e-05 5.516400e-02 9.429768e-01

|

1

2

3

4

|

best_solnp_loglik <- base_mdl$best_estimates$solnp["LogL"]

# Print best rugarch results

head(base_mdl$best_estimates$rugarch, -1)

|

1

2

3

4

5

6

|

## mu omega alpha beta se_mu

## 4.733879e-04 1.631421e-06 5.825871e-02 9.312543e-01 1.190809e-04

## se_omega se_alpha se_beta se_robust_mu se_robust_omega

## NaN NaN NaN 2.845166e-04 2.029449e-05

## se_robust_alpha se_robust_beta

## 2.484959e-01 2.635755e-01

|

1

|

best_rugarch_loglik <- base_mdl$best_estimates$rugarch["LogL"]

|

Then, we estimate higher-order model sGARCH(2,1):

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

|

# Set bounds for GARCH-N

lw_bs <- c(-0.05, 1e-08, 1e-06, 1e-06, 1e-6) # [mu, omega, alpha1, beta1, beta2]

up_bs <- c(0.1, 0.3, 0.2, 0.2, 0.85) # [mu, omega, alpha1, beta1, beta2]

if (!file.exists("Data/KO_GARCH_sg21_mdl.rds")) {

## 5. Re-estimate GARCH (Multi-Start) ----

sg21_mdl <- estimate_garch_dynamic(

y = y,

n_starts = 10, # change number of random starts here, better set to 100

garch_order = c(2,1),

model_type = "sGARCH", # choose model

distribution = "norm", # choose error distribution

lower_bounds = lw_bs,

upper_bounds = up_bs,

loglik_func = Likelihood.GARCH,

ineq_constraints = Inequality.constraints.GARCH,

custom_control = control.solnp

)

# Save results

saveRDS(sg21_mdl, file = "Data/KO_GARCH_sg21_mdl.rds")

} else {

# Access saved data

sg21_mdl <- readRDS("Data/KO_GARCH_sg21_mdl.rds")

}

|

1

2

3

4

5

|

# Find best fits

best_solnp_idx <- which.max(sg21_mdl$solnp_results[, "LogL"])

best_rugarch_idx <- which.max(sg21_mdl$rugarch_results[, "LogL"])

# Print best SOLNP results

head(sg21_mdl$best_estimates$solnp, -1)

|

1

2

|

## mu omega alpha1 alpha2 beta

## 6.781344e-04 9.122594e-05 1.730226e-01 1.092850e-01 1.092859e-01

|

1

2

3

4

|

sg21_best_solnp_loglik <- sg21_mdl$best_estimates$solnp["LogL"]

# Print best rugarch results

head(sg21_mdl$best_estimates$rugarch, -1)

|

1

2

3

4

5

6

7

8

|

## mu omega alpha1 alpha2

## 4.781701e-04 1.624803e-06 5.840805e-02 4.891468e-08

## beta se_mu se_omega se_alpha1

## 9.311935e-01 1.197180e-04 NaN 1.117900e-02

## se_alpha2 se_beta se_robust_mu se_robust_omega

## 5.959924e-03 NaN 1.369747e-04 3.679863e-06

## se_robust_alpha1 se_robust_alpha2 se_robust_beta

## 2.758160e-02 8.551859e-02 6.484744e-02

|

1

|

sg21_best_rugarch_loglik <- sg21_mdl$best_estimates$rugarch["LogL"]

|

1

2

3

4

5

6

7

8

9

|

ll_restricted <- best_solnp_loglik # GARCH(1,1)

ll_unrestricted <- sg21_best_solnp_loglik # GARCH(2,1)

p_restricted <- 4 # Number of parameters in restricted model

p_unrestricted <- 5 # Number of parameters in unrestricted model

# LRT

lr_stat <- 2 * (ll_unrestricted - ll_restricted)

p_value <- 1 - pchisq(lr_stat, p_unrestricted - p_restricted)

cat("LR =", round(lr_stat, 3), ", p =", round(p_value, 4), ", Decision:", ifelse(p_value < 0.05, "REJECT H0 (unrestricted better)", "FAIL TO REJECT H0 (restricted adequate)"), "\n")

|

1

|

## LR = -9911.39 , p = 1 , Decision: FAIL TO REJECT H0 (restricted adequate)

|

The LRT implies that simpler model provide a better estimate for our dataset, hence we will apply this specification for the estimate of required models: GARCH-N, GARCH-t, EGARCH and GJR-GARCH-N.

ii. GARCH-N Estimate#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

|

if (!file.exists("Data/KO_GARCH_gn_mdl.rds")) {

gn_mdl <- estimate_garch_dynamic(

y = y,

n_starts = 10, # change number of random starts here, better set to 100

garch_order = c(1,1),

model_type = "GARCH-N", # choose model

distribution = "norm", # choose error distribution

lower_bounds = lb.GARCH,

upper_bounds = ub.GARCH,

loglik_func = Likelihood.GARCH,

ineq_constraints = Inequality.constraints.GARCH,

custom_control = control.solnp

)

# Save results

saveRDS(gn_mdl, file = "Data/KO_GARCH_gn_mdl.rds")

} else {

# Access saved data

gn_mdl <- readRDS("Data/KO_GARCH_gn_mdl.rds")

}

|

1

2

3

4

|

# Extract best parameter estimate & best fit model

gn_best_fit <- gn_mdl$best_models

gn_best_rugarch_pars <- head(gn_mdl$best_estimates$solnp,-1)

gn_best_rugarch_pars

|

iii. GARCH-t Estimate#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

|

# GARCH-t bounds

# Parameter order: [mu, omega, alpha1, beta1, nu]

lwb <- c(-0.1, 1e-6, 1e-6, 1e-6, 2.1)

upb <- c( 0.1, 0.1, 0.3, 0.95, 30.0)

if (!file.exists("Data/KO_GARCH_gt_mdl.rds")) {

gt_mdl <- estimate_garch_dynamic(

y = y,

n_starts = 10, # change number of random starts here, better set to 100

garch_order = c(1,1),

model_type = "GARCH-t", # choose model

distribution = "norm", # choose error distribution

lower_bounds = lwb,

upper_bounds = upb,

loglik_func = Likelihood.GARCH,

ineq_constraints = Inequality.constraints.GARCH,

custom_control = control.solnp

)

# Save results

saveRDS(gt_mdl, file = "Data/KO_GARCH_gt_mdl.rds")

} else {

# Access saved data

gt_mdl <- readRDS("Data/KO_GARCH_gt_mdl.rds")

}

# Extract model data

gt_best_fit <- gt_mdl$best_models

gt_best_rugarch_pars <- gt_mdl$best_estimates$rugarch[1:5]

gt_best_rugarch_pars

|

iv. EGARCH Estimate#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

|

# EGARCH Bounds

# Parameter order: [mu, omega, alpha1, gamma1, beta1]

eg_lb <- c(-0.1, -2.0, -1.0, -1.0, -0.99)

eg_up <- c( 0.1, 0.5, 1.0, 1.0, 0.99)

if (!file.exists("Data/KO_GARCH_eg_mdl.rds")) {

eg_mdl <- estimate_garch_dynamic(

y = y,

n_starts = 10, # change number of random starts here, better set to 100

garch_order = c(1,1),

model_type = "EGARCH", # choose model

distribution = "norm", # choose error distribution

lower_bounds = eg_lb,

upper_bounds = eg_up,

loglik_func = Likelihood.GARCH,

ineq_constraints = Inequality.constraints.GARCH,

custom_control = control.solnp

)

# Save results

saveRDS(eg_mdl, file = "Data/KO_GARCH_eg_mdl.rds")

} else {

# Access saved data

eg_mdl <- readRDS("Data/KO_GARCH_eg_mdl.rds")

}

# Extract model data

eg_best_fit <- eg_mdl$best_models

eg_best_rugarch_pars <- eg_mdl$best_estimates$rugarch[1:5]

eg_best_rugarch_pars

|

v. GJR-GARCH-N Estimate#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

|

# GJR-GARCH-N bounds

# Parameter order: [mu, omega, alpha1, gamma1, beta1]

gjr_lb <- c(-0.1, 1e-6, 1e-6, 1e-6, 1e-6)

gjr_ub <- c( 0.1, 0.1, 0.3, 0.5, 0.95)

if (!file.exists("Data/KO_GARCH_gjrgn_mdl.rds")) {

gjrgn_mdl <- estimate_garch_dynamic(

y = y,

n_starts = 10, # change number of random starts here, better set to 100

garch_order = c(1,1),

model_type = "GJR-GARCH-N", # choose model

distribution = "norm", # choose error distribution

lower_bounds = gjr_lb,

upper_bounds = gjr_ub,

loglik_func = Likelihood.GARCH,

ineq_constraints = Inequality.constraints.GARCH,

custom_control = control.solnp

)

# Save results

saveRDS(gjrgn_mdl, file = "Data/KO_GARCH_gjrgn_mdl.rds")

} else {

# Access saved data

gjrgn_mdl <- readRDS("Data/KO_GARCH_gjrgn_mdl.rds")

}

# Extract model data

gjrgn_best_fit <- gjrgn_mdl$best_models

gjrgn_best_rugarch_pars <- gjrgn_mdl$best_estimates$rugarch[1:5]

gjrgn_best_rugarch_pars

|

vi. Result Comparison & Plots#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

|

# Get all unique parameter names

all_params <- unique(c(

names(gn_best_rugarch_pars),

names(gt_best_rugarch_pars),

names(eg_best_rugarch_pars),

names(gjrgn_best_rugarch_pars)

))

# Create empty matrix

results_matrix <- matrix(NA, nrow = 4, ncol = length(all_params))

rownames(results_matrix) <- c("GARCH-N", "GARCH-t", "EGARCH", "GJR-GARCH-N")

colnames(results_matrix) <- all_params

# Fill in the values

for (param in names(gn_best_rugarch_pars)) {

results_matrix["GARCH-N", param] <- gn_best_rugarch_pars[param]

}

for (param in names(gt_best_rugarch_pars)) {

results_matrix["GARCH-t", param] <- gt_best_rugarch_pars[param]

}

for (param in names(eg_best_rugarch_pars)) {

results_matrix["EGARCH", param] <- eg_best_rugarch_pars[param]

}

for (param in names(gjrgn_best_rugarch_pars)) {

results_matrix["GJR-GARCH-N", param] <- gjrgn_best_rugarch_pars[param]

}

# Convert to data frame

results_df <- as.data.frame(results_matrix)

names(results_df)[names(results_df) == "shape"] <- "nu"

print((results_df))

|

1

2

3

4

5

6

7

8

9

10

|

## mu omega alpha beta nu

## GARCH-N 0.0002967198 7.560890e-05 0.12667254 0.8233275 NA

## GARCH-t 0.0004948997 1.533138e-06 0.06400793 0.9266939 4.973822

## EGARCH 0.0002579436 -1.158257e-01 -0.04981127 0.9863477 NA

## GJR-GARCH-N 0.0003411014 1.688795e-06 0.02709499 0.9307542 NA

## gamma

## GARCH-N NA

## GARCH-t NA

## EGARCH 0.12945606

## GJR-GARCH-N 0.06202623

|

1

2

3

4

|

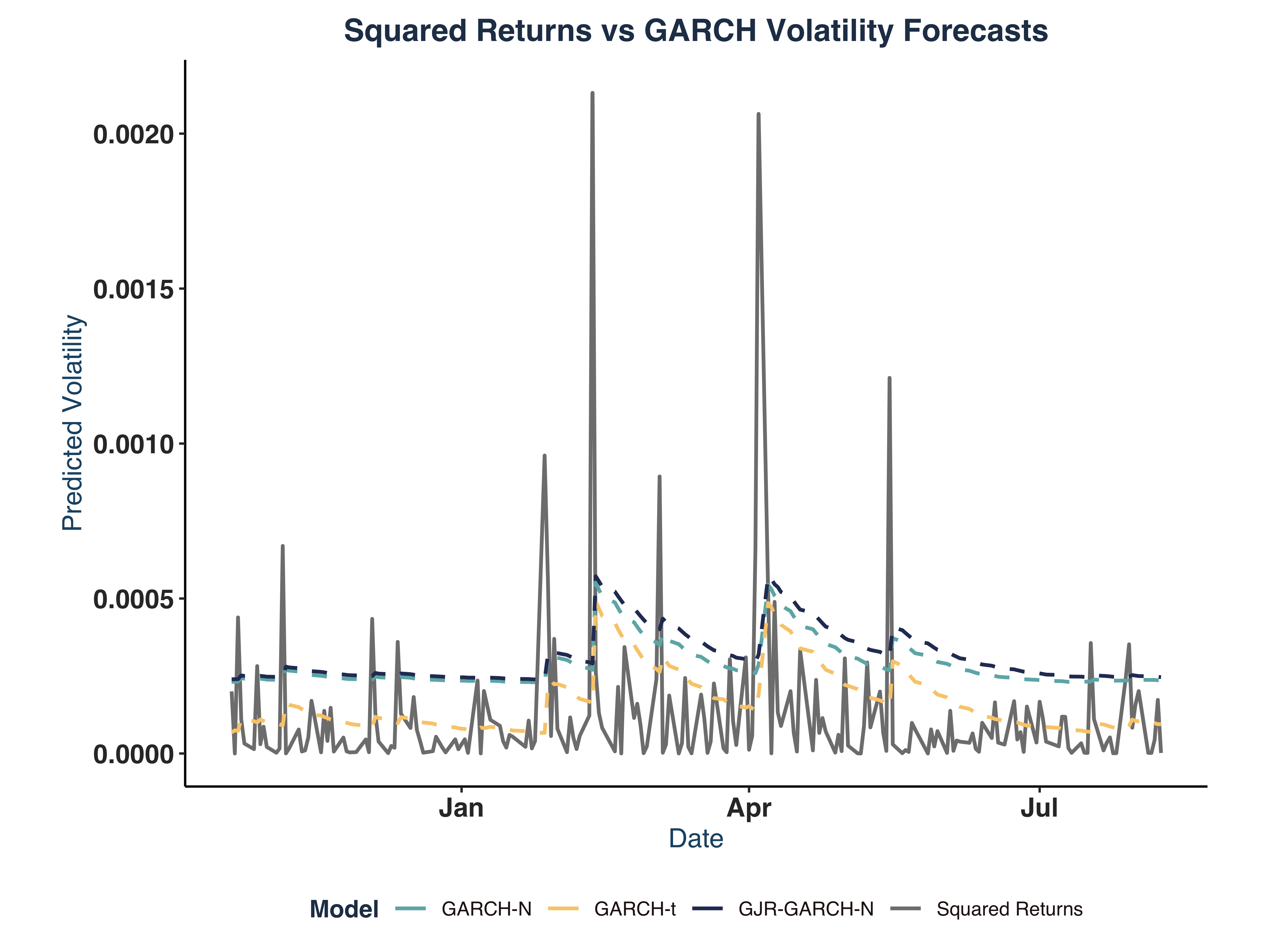

log_ret_plot <- plot_return_derivatives(

KO_daily, ticker_name = "KO",

plot_width = 6, plot_height = 3)

log_ret_plot$logret

|

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

|

## Simulate series for estimated models

# Get number observations

T_obs <- length(log_ret_real)

# Create matrix of sigma values across models

sig_KO <- cbind(

rugarch::sigma(gn_best_fit$rugarch),

rugarch::sigma(gt_best_fit$rugarch),

rugarch::sigma(eg_best_fit$rugarch),

rugarch::sigma(gjrgn_best_fit$rugarch)

)

colnames(sig_KO) <- c("GARCH-N", "GARCH-t", "EGARCH", "GJR-GARCH-N")

# Create plot data

plot_data <- cbind("Squared Returns" = KO_daily$sqret, sig_KO)

# Create time series object with actual dates

ts_data <- ts(plot_data,

start = c(year(min(KO_daily$date)), yday(min(KO_daily$date))),

frequency = 365.25)

# Plot all series

colors <- c("Squared.Returns" = "gray40",

"GARCH.N" = "#663171FF",

"GARCH.t" = "#EA7428FF",

"EGARCH" = "#0C7156FF",

"GJR.GARCH.N" = "#3A507FFF")

sim_plot <- autoplot(ts_data) +

scale_color_manual(values = colors)+

theme(axis.line = element_line(colour = "black"),

panel.grid.major = element_blank(),

panel.grid.minor = element_blank(),

panel.border = element_blank(),

panel.background = element_blank(),

legend.position = "bottom"

) +

global_fonts+

labs(

title = "Conditional Volatility across Estimated Models",

x = "Date",

y = "Volatility / Squared Returns",

color = "Model"

)

print(sim_plot)

|

vii. Evidence of Excessive Kurtosis & Skewness#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

|

# Extact standardized residuals

std_resid_gn <- rugarch::residuals(gn_best_fit$rugarch, standardize = TRUE)

std_resid_gt <- rugarch::residuals(gt_best_fit$rugarch, standardize = TRUE)

std_resid_eg <- rugarch::residuals(eg_best_fit$rugarch, standardize = TRUE)

std_resid_gjr <- rugarch::residuals(gjrgn_best_fit$rugarch, standardize = TRUE)

# Helper function to extract test result

get_jb_results <- function(residuals) {

jb_test <- jarque.bera.test(residuals)

return(c(

JB_Statistic = as.numeric(jb_test$statistic),

JB_p_value = as.numeric(jb_test$p.value)

))

}

# Create the residuals list

residuals_list <- list(std_resid_gn, std_resid_gt, std_resid_eg, std_resid_gjr)

# Create the data frame of kurtosis, excess kurtosis, and test results

kurtosis_results <- data.frame(

Model = c("GARCH-N", "GARCH-t", "EGARCH", "GJR-GARCH-N"),

Kurtosis = c(kurtosis(std_resid_gn), kurtosis(std_resid_gt),

kurtosis(std_resid_eg), kurtosis(std_resid_gjr)),

Excess_Kurtosis = c(kurtosis(std_resid_gn)-3, kurtosis(std_resid_gt)-3,

kurtosis(std_resid_eg)-3, kurtosis(std_resid_gjr)-3),

JB_Statistic = sapply(residuals_list, function(x) get_jb_results(x)[1]),

JB_p_value = sapply(residuals_list, function(x) get_jb_results(x)[2])

)

print(kurtosis_results)

|

1

2

3

4

5

|

## Model Kurtosis Excess_Kurtosis JB_Statistic JB_p_value

## 1 GARCH-N 8.590343 5.590343 8562.986 0

## 2 GARCH-t 8.721817 5.721817 8967.117 0

## 3 EGARCH 8.467178 5.467178 8187.392 0

## 4 GJR-GARCH-N 8.407663 5.407663 8027.130 0

|

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

|

# Calculate skewness of volatility

skewness_results <- data.frame(

Volatility_Skewness = apply(sig_KO, 2, skewness)

)

# Test statistical significance of skewness

skewness_tests <- apply(sig_KO, 2, function(x) {

# Skewness test (H0: skewness = 0)

n <- length(x)

skew_stat <- skewness(x)

se_skew <- sqrt(6/n) # Standard error of skewness

z_stat <- skew_stat / se_skew

p_value <- 2 * (1 - pnorm(abs(z_stat)))

return(c(skewness = skew_stat, z_statistic = z_stat, p_value = p_value))

})

skewness_test_results <- data.frame(t(skewness_tests))

print(skewness_test_results)

|

1

2

3

4

5

|

## skewness z_statistic p_value

## GARCH-N 2.622833 85.91529 0

## GARCH-t 2.630862 86.17830 0

## EGARCH 2.410865 78.97192 0

## GJR-GARCH-N 2.613715 85.61663 0

|

The test results show clear evidence of both excessive kurtosis and skewness in estimated models.

Moreover, it is clear that the highest volatility period is around 2013-2014, which seems to coincide with the declining soda consumption at the time.

c. Estimate 2.5% VaR & ES#

i. Estimation#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

|

# Specs Setup

n_IS <- 4000 # no. simulation

alpha <- 0.025 # 2.5% VaR

date_sr <- KO_daily$date # Date labels

# Check if there exist saved model data

if (!file.exists("Data/KO_Residuals.rds")) {

KO_res <- Estimate.VaR.ES.models(ret = log_ret_real,

alpha = alpha,

n_IS = n_IS,

date = date_sr)

# Save model data

saveRDS(KO_res, file = "Data/KO_Residuals.rds")

# Extrac estimated dataset

KO_qe_dt <- as.data.frame(KO_res$VaR.ES.df)

} else {

# Access saved model data

KO_res <- readRDS("Data/KO_Residuals.rds")

KO_qe_dt <- as.data.frame(KO_res$VaR.ES.df)

}

# Print some observations

tail(KO_qe_dt,5)

|

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

|

## date ret q_GARCH_N e_GARCH_N hit_GARCH_N q_GARCH_t e_GARCH_t

## 2434 2025-08-04 0.1451146 -2.143210 -2.556375 FALSE -2.088496 -2.491113

## 2435 2025-08-05 0.1304311 -2.073038 -2.472675 FALSE -2.033012 -2.424932

## 2436 2025-08-06 0.6639734 -2.006067 -2.392793 FALSE -1.979413 -2.361001

## 2437 2025-08-07 1.3148655 -1.971980 -2.352136 FALSE -1.952074 -2.328392

## 2438 2025-08-08 -0.1278738 -2.028638 -2.419716 FALSE -1.998845 -2.384179

## hit_GARCH_t q_GJRGARCH_t e_GJRGARCH_t hit_GJRGARCH_t q_RiskMetrics

## 2434 FALSE -2.111282 -2.518292 FALSE -2.003095

## 2435 FALSE -2.048532 -2.443445 FALSE -1.943322

## 2436 FALSE -1.988499 -2.371839 FALSE -1.885161

## 2437 FALSE -1.941655 -2.315965 FALSE -1.855321

## 2438 FALSE -1.929409 -2.301357 FALSE -1.906349

## e_RiskMetrics hit_RiskMetrics q_HistSim e_HistSim hit_HistSim q_GAS1F

## 2434 -2.389249 FALSE -2.050224 -2.706837 FALSE -1.721901

## 2435 -2.317953 FALSE -2.050224 -2.706837 FALSE -1.700777

## 2436 -2.248579 FALSE -2.050224 -2.706837 FALSE -1.680579

## 2437 -2.212986 FALSE -2.050224 -2.706837 FALSE -1.661259

## 2438 -2.273851 FALSE -2.050224 -2.706837 FALSE -1.642771

## e_GAS1F hit_GAS1F q_GAS2F e_GAS2F hit_GAS2F q_CAREAS e_CAREAS

## 2434 -2.889322 FALSE -1.849358 -2.824393 FALSE -2.545021 -3.596716

## 2435 -2.853876 FALSE -1.819951 -2.796986 FALSE -2.294611 -3.346305

## 2436 -2.819985 FALSE -1.791847 -2.770399 FALSE -2.085626 -3.137320

## 2437 -2.787566 FALSE -1.764991 -2.744610 FALSE -1.956230 -3.007925

## 2438 -2.756544 FALSE -1.739330 -2.719597 FALSE -1.902551 -2.954245

## hit_CAREAS q_CARESAV e_CARESAV hit_CARESAV q_GAS_t e_GAS_t hit_GAS_t

## 2434 FALSE -2.478974 -3.502481 FALSE -2.295290 -3.084985 FALSE

## 2435 FALSE -2.303023 -3.326529 FALSE -2.210291 -2.969971 FALSE

## 2436 FALSE -2.141791 -3.165298 FALSE -2.129779 -2.862278 FALSE

## 2437 FALSE -2.117940 -3.141447 FALSE -2.082508 -2.789670 FALSE

## 2438 FALSE -2.243956 -3.267463 FALSE -2.165320 -2.908771 FALSE

|

ii. VaR Analysis#

Estimated parameters:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

|

## Extract estimated parameters of interested models ----

# Declare list of models of interest

mdl_ls <- c("GARCH_N", "GJRGARCH_t", "CAREAS", "CARESAV", "GAS1F") # HistSim is non-parametric

# Model Names

mdl_names <- c("GARCH_N", "GJR_GARCH_t", "AS_CAViaR", "SAV_CAViaR", "GAS_1F")

# Assign empty result list

param_ests <- list()

# Extract estimated parameters

for (i in 1:length(mdl_ls)) {

name <- mdl_names[i]

model <- mdl_ls[i]

param_ests[[name]] <- KO_res$pars[[model]]

}

## Print out results ----

# Define parameter structures for each model

param_structures <- list(

"GARCH_N" = c("omega", "alpha1", "beta1"),

"GJR_GARCH_t" = c("omega", "alpha1", "beta1", "gamma1", "shape"),

"AS_CAViaR" = c("beta1", "beta2", "beta3", "beta4", "gamma1", "gamma2", "gamma3"),

"SAV_CAViaR" = c("beta1", "beta2", "beta3", "gamma1", "gamma2", "gamma3"),

"GAS_1F" = c("beta1", "gamma1", "alpha1", "alpha2")

)

# Get all unique parameter names

all_params <- unique(unlist(param_structures))

# Initialize a result table

param_tbl <- data.frame(Model=mdl_names, stringsAsFactors = FALSE)

for (param in all_params) {

param_tbl[[param]] <- NA

}

# Fill in estimated parameters

for (model in mdl_names) {

# Get row index

row_id <- which(param_tbl$Model == model)

# Get estimated parameters

params <- c(param_ests[[model]]) # vectorise

# Get corresponding names

param_names <- param_structures[[model]]

# Assign values

for (i in 1:length(params)) {

param_tbl[row_id, param_names[i]] <- params[i]

}

}

names(param_tbl)[names(param_tbl) == "shape"] <- "nu"

print(param_tbl)

|

1

2

3

4

5

6

7

8

9

10

11

12

|

## Model omega alpha1 beta1 gamma1 nu beta2

## 1 GARCH_N 0.01761539 0.07101346 0.9196059 NA NA NA

## 2 GJR_GARCH_t 0.01624465 0.02491078 0.9269894 0.08274889 5.562725 NA

## 3 AS_CAViaR NA NA -0.1709521 0.99951219 NA -0.08247883

## 4 SAV_CAViaR NA NA -0.0454307 1.10615824 NA -0.22649243

## 5 GAS_1F NA -1.69858232 0.9678562 0.01190525 NA NA

## beta3 beta4 gamma2 gamma3 alpha2

## 1 NA NA NA NA NA

## 2 NA NA NA NA NA

## 3 -0.4126349 0.8297337 0.01489130 1.1618509 NA

## 4 0.8974376 NA -0.02892479 0.2029524 NA

## 5 NA NA NA NA -2.850194

|

Are the signs as expected?

- GARCH models: all

\(\omega, \alpha, \beta>0\) are as expected. Positive asymmetry (leverage effect) is confirmed with \(\gamma>0\).

- AS-ES-CAViaR model: intercept, absolute negative & positive returns parameters are as expected:

\(\beta_1,\beta_2,\beta_3<0\). However, the unexpected \(\beta_4>0\) can be explained by the volatility clustering behaviour we observed in the graphical analysis in a, i.e. negative loss \(\hat{q}_{1,t-1}<0\) followed by a negative loss.

- SAV-ES-CAViaR model: all parameters are as expected:

\(\beta_1,\beta_2<0\) except \(\beta_3>0\) (same behaviour as above).

- GAS-1F model: all parameters are as expected. In particular,

\(\alpha_1 \leq 0 \in [-2,0]\) - VaR scaling, \(\alpha_2 \leq 0 \in [-3,-1]\) - ES scaling, \(\gamma_1>0\) - score sensitivity, and \(\beta_1>0\) - persistence.

d. ES Analysis#

i. Plot log-return & estimated conditional quantile models#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

|

## Reshape plot data (wide to long) ----

# Extract VaR & ES columns

all_mdl_ls <- c("HistSim", "GARCH_N", "GJRGARCH_t", "CAREAS", "CARESAV", "GAS1F")

all_mdl_names <- c("HistSim_250d", "GARCH_N", "GJR_GARCH_t", "AS_CAViaR", "SAV_CAViaR", "GAS_1F")

plt_cols <- c("date", "ret", paste0("q_", all_mdl_ls), paste0("e_", all_mdl_ls))

KO_qe_plt_dt <- KO_qe_dt[, plt_cols]

# Extract VaR columns & reshape

var_long_dt <- reshape(KO_qe_plt_dt[,c("date", "ret", paste0("q_", all_mdl_ls))],

direction = "long",

idvar = "date",

varying = c("ret", paste0("q_", all_mdl_ls)), v.names = "value",

timevar = "model", times = c("LogRet", all_mdl_names)

)

# Drop row indices

rownames(var_long_dt) <- NULL

mdl_colors <- c("LogRet" = "grey40", "HistSim_250d" = "#C70E7BFF",

"GARCH_N" = "#007BC3FF", "GJR_GARCH_t" = "#54BCD1FF",

"AS_CAViaR" = "#EF7C12FF", "SAV_CAViaR" = "#F4B95AFF",

"GAS_1F"="#009F3FFF")

KO_VaR_plt <- var_long_dt |>

ggplot(aes(x = date, y = value, color = model)) +

geom_line(linewidth = 0.2)+

scale_color_manual(values =mdl_colors)+

theme(panel.grid.major = element_blank(),

panel.grid.minor = element_blank(),

panel.border = element_blank(),

panel.background = element_blank(),

legend.position = "bottom"

) +

global_fonts+

labs(

title = "Log-Returns vs. Estimated Value at Risk",

x = "Date",

y = "Log Returns/VaR",

color = "Model"

)

# Save plot

ggsave(paste0(c("Plots/KO_VaR_plt.pdf")), plot = KO_VaR_plt, width=8, height=6)

# Print

# I recommend the library `plotly` for interactive graph

# ggplotly(KO_VaR_plt, colors = mdl_colors)

KO_VaR_plt

|

ii. Plot ES#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

|

## Reshape plot data (wide to long) ----

# Extract ES columns & reshape

es_long_dt <- reshape(KO_qe_plt_dt[,c("date", "ret", paste0("e_", all_mdl_ls))],

direction = "long",

idvar = "date",

varying = c("ret", paste0("e_", all_mdl_ls)), v.names = "value",

timevar = "model", times = c("LogRet", all_mdl_names)

)

# Drop row indices

rownames(es_long_dt) <- NULL

KO_ES_plt <- es_long_dt |>

ggplot(aes(x = date, y = value, color = model)) +

geom_line(linewidth = 0.2)+

scale_color_manual(values = mdl_colors)+

theme(panel.grid.major = element_blank(),

panel.grid.minor = element_blank(),

panel.border = element_blank(),

panel.background = element_blank(),

legend.position = "bottom"

) +

global_fonts+

labs(

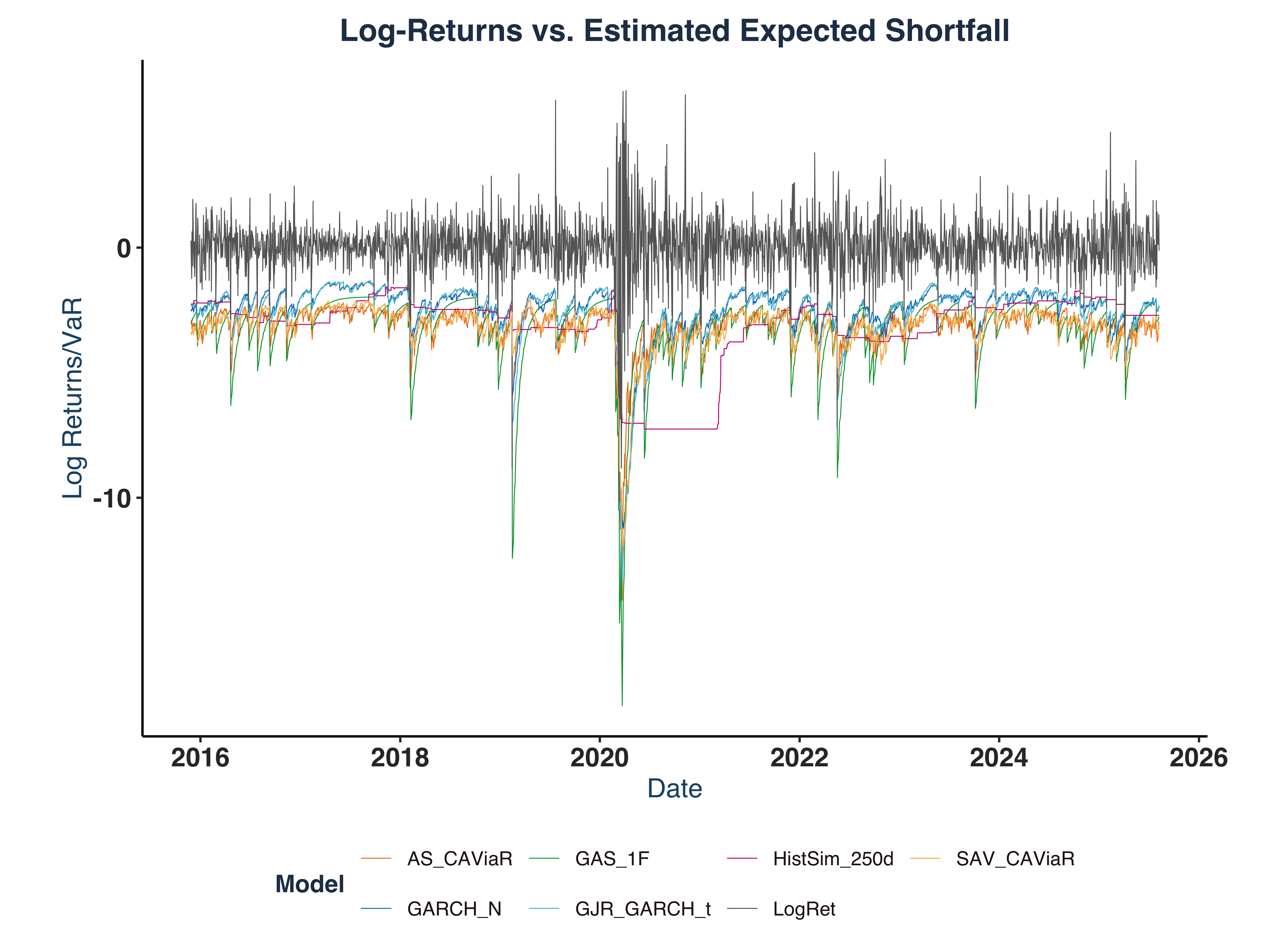

title = "Log-Returns vs. Estimated Expected Shortfall",

x = "Date",

y = "Log Returns/VaR",

color = "Model"

)

# Save plot

ggsave(paste0(c("Plots/KO_ES_plt.pdf")), plot = KO_ES_plt, width=8, height=6)

# Print

# ggplotly(KO_ES_plt) # I recommend the library `plotly` for interactive graph, however it won't compile for pdf export

KO_ES_plt

|

iii. Model Graphical Evaluation#

Plot Main Features:

- A major volatility spike around COVID-19 pandemic, associated with a massive drop by approximately -10%.

- In both VaR and ES plot, all models successfully capture major market volatility.

- GAS-type models seem to be the most responsive model that quickly reflects the market turmoil with sensitive responses, e.g. it predicted a -15.0% drop on 2020-03-13 in response to the -10.2% decline in Log-return on 2020-03-12.

Detailed Models Evaluation:

- GAS-1F: the most responsive model with largest adjustment during volatile periods. It also shows a smooth adaptation post-crisis.

- AS-CAViaR: the second most responsive model most of the time, associated with sharp responses; however, it is sometimes hypersensitive. For example, it estimated a -14.8% decrease in VaR on 2020-03-23 while the realized decline was only -2.0%.

- SAV-CAViaR: a balanced model which is neither too reactive nor too static.

- GARCH-N: a stable, consistent model displaying less noise during calm periods. It also exhibits smoother trajectories than CAViaR-type models.

- GJR-GARCH-t: same as GARCH-N but shows less discontinuity (better smoothness).

- HistSim-250d: an unresponsive model showing slow responses to crises. Poor performance in both volatile & quiet periods.

Which model to choose in which period?

- In volatile periods, GAS-1F shows exceptional responsiveness, which helps capture the tail risks effectively, reduce react time, and mitigate foreseeable losses.

- In calmer periods, GARCH-type models are suitable candidate for stable estimates, which lower possibly false signals and reduce unnecessary trading costs.

e. Compute the Hit-ratio for the conditional quantile models.#

i. Hit Ratio Computation#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

|

# Extract HITS variables

KO_hit_dt <- select(KO_qe_dt, paste0("hit_",all_mdl_ls))

# Calculate hit ratios

n_est <- nrow(KO_qe_dt)

KO_hit_ratio <- KO_hit_dt %>%

summarise_all(sum) %>% # column-wise sum

mutate_all(\(x) x / n_est) %>% # anonymous function syntax since R 4.1+

`colnames<-`(all_mdl_names) %>% # assign column names

pivot_longer(

cols = everything(),

names_to = "Model",

values_to = "Hit_Ratio"

)

print(KO_hit_ratio)

|

1

2

3

4

5

6

7

8

9

|

## # A tibble: 6 × 2

## Model Hit_Ratio

## <chr> <dbl>

## 1 HistSim_250d 0.0304

## 2 GARCH_N 0.0254

## 3 GJR_GARCH_t 0.0242

## 4 AS_CAViaR 0.0246

## 5 SAV_CAViaR 0.0242

## 6 GAS_1F 0.0320

|

ii. Conclusion#

Based on hit ration calculation, I would prefer GJR-GARCH-t model because of its lowest hit ratio.

Exercise 2 - Simulation Exercises#

a. Time Series Examination#

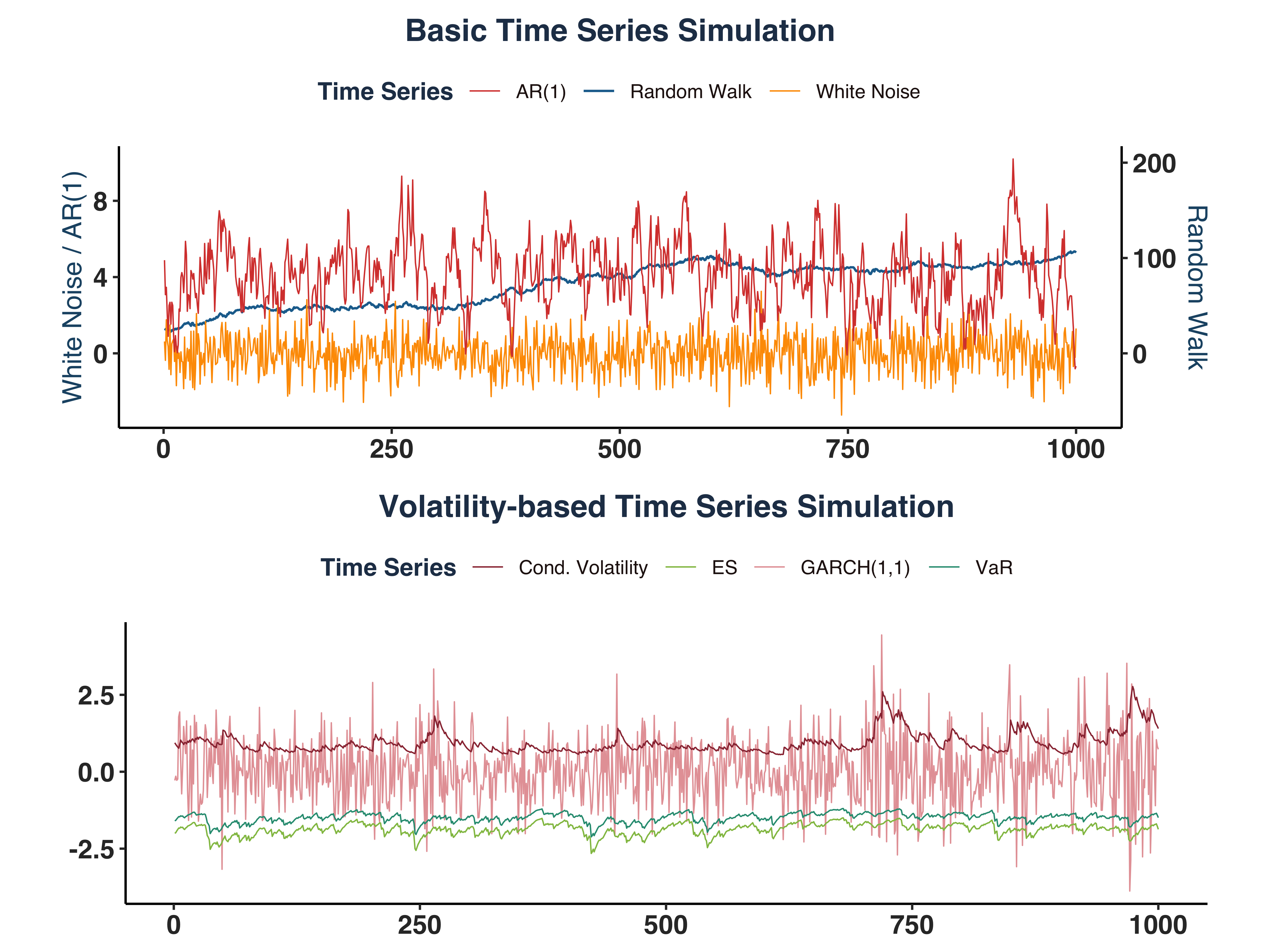

Given five processes:

\(Y_t = Y_{t-1} + \varepsilon_t\): Non-stationary random walk, used as a reference for forecasting, acting as the “best” prediction we can make.\(Y_t = \varepsilon_t\): Stationary White Noise, which is the “best” forecast error we can (hopefully) get \(\varepsilon_t = Y_t - \hat{Y_t}\).\(Y_t = 0.8 + 0.8Y_{t-1} + \varepsilon_t\): Stationary AR(1) process, which can be a candidate model for financial series modelling, a state-space representation of a ARMA(p,q) process, or a case of unit root testing.\(Y_t = \sigma_t\varepsilon_t, \quad \sigma_t^2 = 0.04 + 0.05Y_{t-1}^2 + 0.90\sigma_t^2\): \(Y_t\) itself is not stationary, but the conditional volatility \(\sigma_t\) is. This GARCH(1,1) model captures time-varying risk in financial returns.\(q_t = \sigma_tz_{0.05} \quad \text{and} \quad e_t = \sigma_t\xi_{0.05}\): Stationary 5% VaR & ES, which capture the extreme (negative) tail risk.

b. Process Simulation#

i. Simulate Processes & Plot#

Simulate five processess:

1

2

3

4

5

6

7

8

9

10

11

12

|

set.seed(1340)

ts_rw <- ARMA.sim(1000, 1,0,0)

ts_wn <- ARMA.sim(1000, 0,0,0)

ts_ar1 <- ARMA.sim(1000, 0.8,0,0.8)

ts_garch1 <- GARCH.sim(1000, 0.04, 0.05, 0.9)

ts_eq <- VaR.ES.sim(1000, 0.05, 0.04, 0.05, 0.9)

# Create plot data

ts_plot_dt <- data.frame(time = 1:1000, ts_rw = ts_rw, ts_wn = ts_wn,

ts_ar1 = ts_ar1, ts_garch1_y = ts_garch1$y,

ts_garch1_sig = ts_garch1$sigma.2,

ts_var = ts_eq$q_t, ts_es = ts_eq$e_t)

|

And plot them:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

|

ts_basic_plt <- ggplot(ts_plot_dt, aes(x=time)) +

geom_line(aes(y=ts_rw*0.05, colour = "Random Walk"),size=0.5) + # Put to secondary y-axis

geom_line(aes(y=ts_wn, colour = "White Noise"),size=0.3) +

geom_line(aes(y=ts_ar1, colour = "AR(1)"),size=0.3) +

scale_y_continuous(

name = "White Noise / AR(1)",

sec.axis = sec_axis(trans = ~ . / 0.05,name = "Random Walk")

) +

theme(panel.grid.major = element_blank(),

panel.grid.minor = element_blank(),

panel.border = element_blank(),

panel.background = element_blank()) +

global_fonts+

labs(title = "Basic Time Series Simulation",x = NULL,y = NULL) +

scale_color_manual(name = "Time Series",

values = c("Random Walk" = "#1F6E9CFF",

"White Noise" = "#FE9B00FF",

"AR(1)" = "#D8443CFF"))

ts_garch_plt <- ggplot(ts_plot_dt, aes(x=time)) +

geom_line(aes(y=ts_garch1_y, colour = "GARCH(1,1)"),size=0.3) +

geom_line(aes(y=ts_garch1_sig, colour = "Cond. Volatility"),size=0.3) +

geom_line(aes(y=ts_var, colour = "VaR"),size=0.3) +

geom_line(aes(y=ts_es, colour = "ES"),size=0.3) +

theme(panel.grid.major = element_blank(),

panel.grid.minor = element_blank(),

panel.border = element_blank(),

panel.background = element_blank()) +

global_fonts+

labs(title = "Volatility-based Time Series Simulation",x = NULL,y = NULL) +

scale_color_manual(name = "Time Series",

values = c("GARCH(1,1)" = "#E6A2A6FF",

"Cond. Volatility" = "#9B3441FF",

"VaR" = "#2B9B81FF",

"ES" = "#92C051FF"))

sim_ts_plt <- ggarrange(ts_basic_plt, ts_garch_plt, nrow = 2, widths = 8, heights = 6)

# Save plot

ggsave(paste0(c("Plots/Simulated_Time_Series_plt.pdf")), plot = sim_ts_plt, width=8, height=6)

sim_ts_plt

|

ii. Time Series Behaviour#

- Random Walk series shows a clear upward trend over time.

- Both White Noise (WN) & AR(1) series exhibit mean-reverting properties, where WN stations around 0 and AR(1) series’s mean is 4.

- Conditional Variance series is stationary around 0.8.

- VaR series varies around

\(q_t ={\sigma}_t*z_{0.05}\approx 0.8944*-1.6449=\) -1.4712018

- ES series fluctuates around

\(e_t ={\sigma}_t*\xi_{0.05}\approx 0.8944*-2.0627=\) -1.8449464.

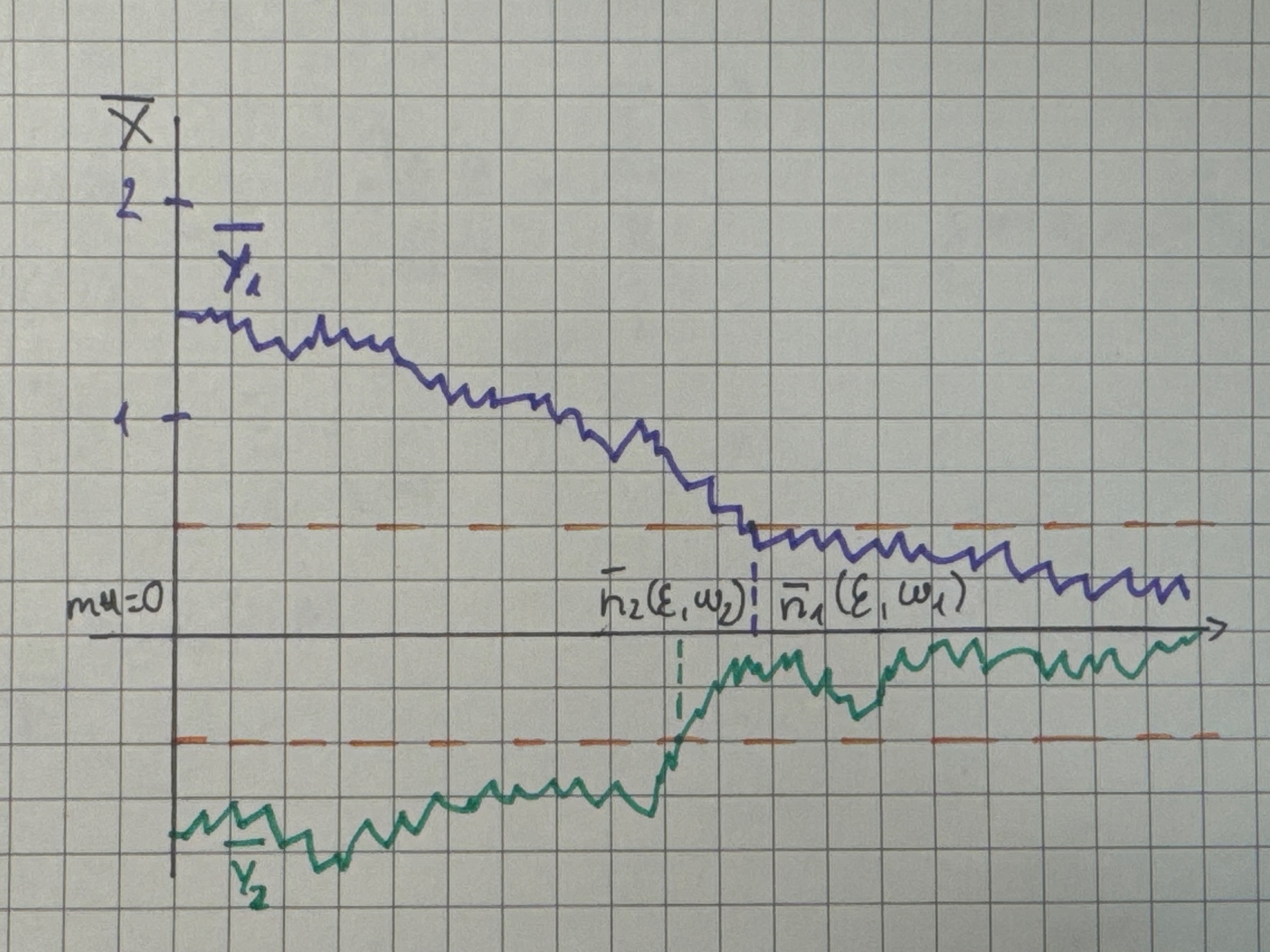

c. Explain Almost Surely (a.s.) Convergence#

-

Intuitively, we can find a bound $\varepsilon > 0 $ that at some point \(n\), the sequence falls under this bound and will never leave it.

-

Formally, a random sequence of sample averages \(\{\bar{Y}_n\}\) converges almost surely if for all \(\omega\in \Omega\) and any \(\varepsilon > 0 \quad \exists \bar{n}(\varepsilon, \omega) \in \mathbb{N}\) such that:

$$

|\bar{Y}_n - \mu| < \varepsilon \quad \forall, n \geq \bar{n}(\varepsilon, \omega)

$$

-

In this context, converging refers to a realization \(\omega\) reverting to its mean \(\mu\).

-

The term \(\bar{n}(\varepsilon, \omega)\) is known as “Convergence Threshold”.

-

Illustration:

{width=60%}

{width=60%}

Note: \(\bar{Y}_1,\bar{Y}_2\) denote different realizations of a time series

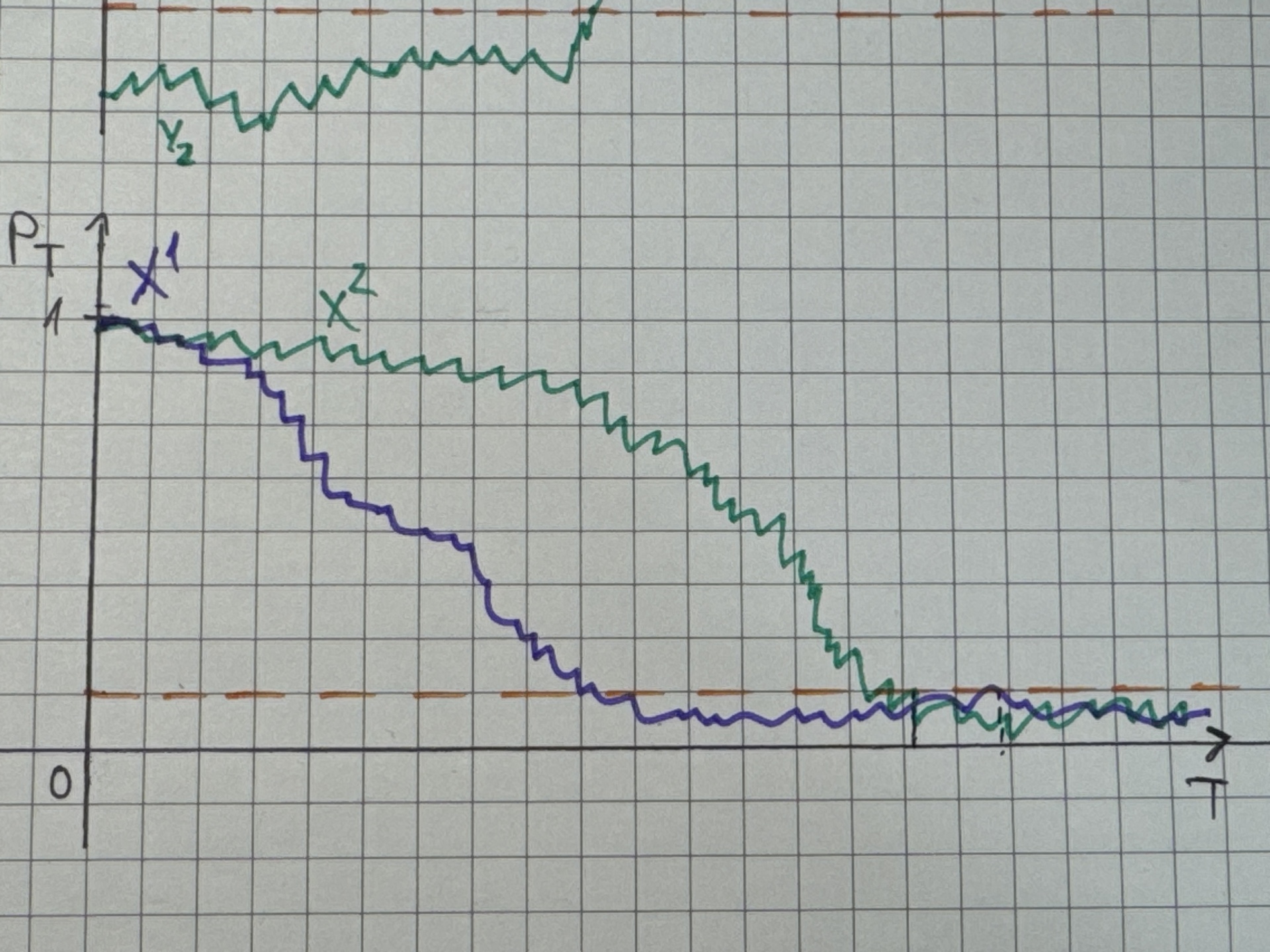

d. Explain Convergence in Probability#

- Intuitively, if we assess the probability that the series falls under the defined bound and never go out:

\(\lim_{n\to \infty} p_n = \lim_{n\to \infty} P\left( |\bar X_n - \mu| > \varepsilon\right)=0\)

- Formally, a sequence of random variables

\(\{X_n\}\) is said to converge in probability to a random variable \(X\) if for any \(\varepsilon>0\):

$$

\lim_{n\to \infty} P\left( | X_n - X| > \varepsilon\right)=0

$$

- In this context,

\(p_n = p_T\) means the probability of absolute deviation between \(\bar{X}_T\) and the limit/mean \(\mu\) by more than \(\varepsilon\) equals to zero at time \(T\).

- In common sense, the probability of getting an out-of-hand observation collapses to zero as sample size grow.

- Demonstration:

{width=60%}

{width=60%}

Note: \(X^1,X^2\) denote different time series

e. Simulation & Convergence#

i. Simulate Stationary Processes#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

|

# Simulate the time series

set.seed(1340)

T_obs <- 10000

sta_ts_wn <- ARMA.sim(T_obs, 0,0,0, ensembles = 4)

sta_ts_ar1 <- ARMA.sim(T_obs, 0.8,0,0.8, ensembles = 4)

sta_ts_garch11 <- GARCH.sim(T_obs, 0.04, 0.05, 0.9, ensembles = 4)

sta_ts_eq <- VaR.ES.sim(T_obs, 0.05, 0.04, 0.05, 0.9, ensembles = 4)

# Compute sequence of averages

mean_wn <- as.data.frame(apply(sta_ts_wn, 2, \(x) cumsum(x)/seq_along(x)))

mean_ar1 <- as.data.frame(apply(sta_ts_ar1, 2, \(x) cumsum(x)/seq_along(x)))

mean_g11 <- as.data.frame(apply(sta_ts_garch11$sigma.2, 2, \(x) cumsum(x)/seq_along(x)))

mean_qt <- as.data.frame(apply(sta_ts_eq$q_t, 2, \(x) cumsum(x)/seq_along(x)))

mean_et <- as.data.frame(apply(sta_ts_eq$e_t, 2, \(x) cumsum(x)/seq_along(x)))

# Compute deviations

eps <- 0.01

abs_dev_wn_dt <- as.data.frame(abs(mean_wn-0)) # mu=0

abs_dev_ar1_dt <- as.data.frame(abs(mean_ar1-4)) # mu=4

abs_dev_g11_dt <- as.data.frame(abs(mean_g11-0.8)) # mu=0.8

mu_var <- sqrt(0.8)*qnorm(0.05, 0, 1)

abs_dev_qt_dt <- as.data.frame(abs(mean_qt-mu_var)) # mu=-1.4712

mu_es <- sqrt(0.8)*(-dnorm(qnorm(0.05, 0, 1), 0, 1) / 0.05)

abs_dev_et_dt <- as.data.frame(abs(mean_et-mu_es)) # mu=-1.8449

# Set names

col_names <- c("Ensemble_1","Ensemble_2","Ensemble_3","Ensemble_4")

list2env(lapply(mget(c("mean_wn", "mean_ar1", "mean_g11","mean_qt", "mean_et")),

\(x) setNames(x, col_names)), envir = .GlobalEnv)

|

1

|

## <environment: R_GlobalEnv>

|

1

2

3

|

list2env(lapply(mget(c("abs_dev_wn_dt", "abs_dev_ar1_dt", "abs_dev_g11_dt",

"abs_dev_qt_dt", "abs_dev_et_dt")),

\(x) setNames(x, col_names)), envir = .GlobalEnv)

|

1

|

## <environment: R_GlobalEnv>

|

1

2

3

|

# Create plot data

list2env(lapply(mget(c("mean_wn", "mean_ar1", "mean_g11","mean_qt", "mean_et")),

\(x) cbind(Index = seq_len(T_obs), x)), envir = .GlobalEnv)

|

1

|

## <environment: R_GlobalEnv>

|

1

2

|

# Print out a series to check

tail(mean_ar1, 10)

|

1

2

3

4

5

6

7

8

9

10

11

|

## Index Ensemble_1 Ensemble_2 Ensemble_3 Ensemble_4

## 9991 9991 4.030821 3.916929 4.005732 3.940538

## 9992 9992 4.031012 3.916674 4.005941 3.940475

## 9993 9993 4.031150 3.916485 4.006032 3.940537

## 9994 9994 4.031361 3.916428 4.006151 3.940445

## 9995 9995 4.031575 3.916271 4.006427 3.940344

## 9996 9996 4.031858 3.916241 4.006735 3.940357

## 9997 9997 4.032243 3.916395 4.007083 3.940438

## 9998 9998 4.032407 3.916415 4.007275 3.940424

## 9999 9999 4.032550 3.916517 4.007449 3.940347

## 10000 10000 4.032733 3.916576 4.007534 3.940287

|

ii. Illustrate a.s.-convergence#

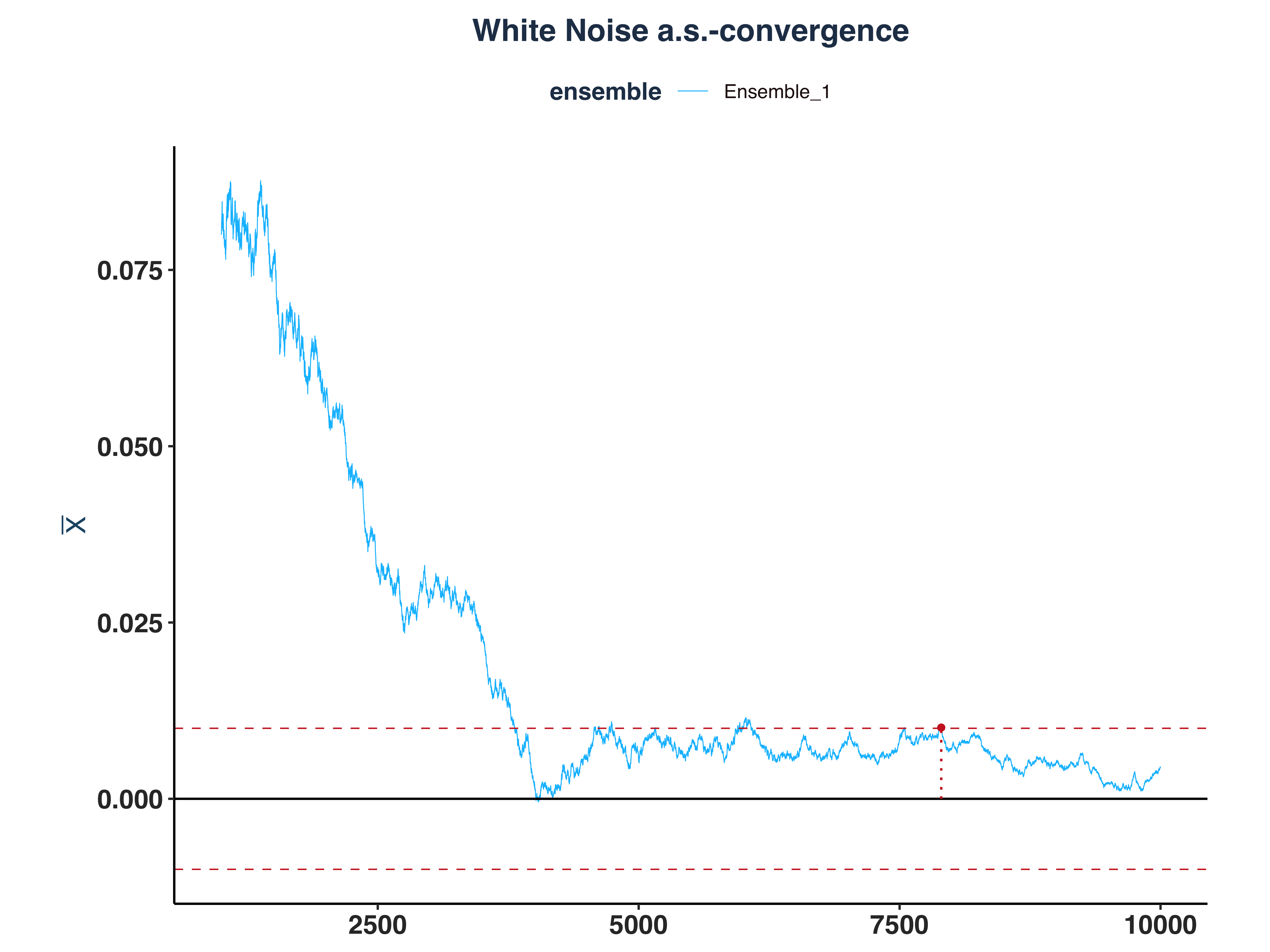

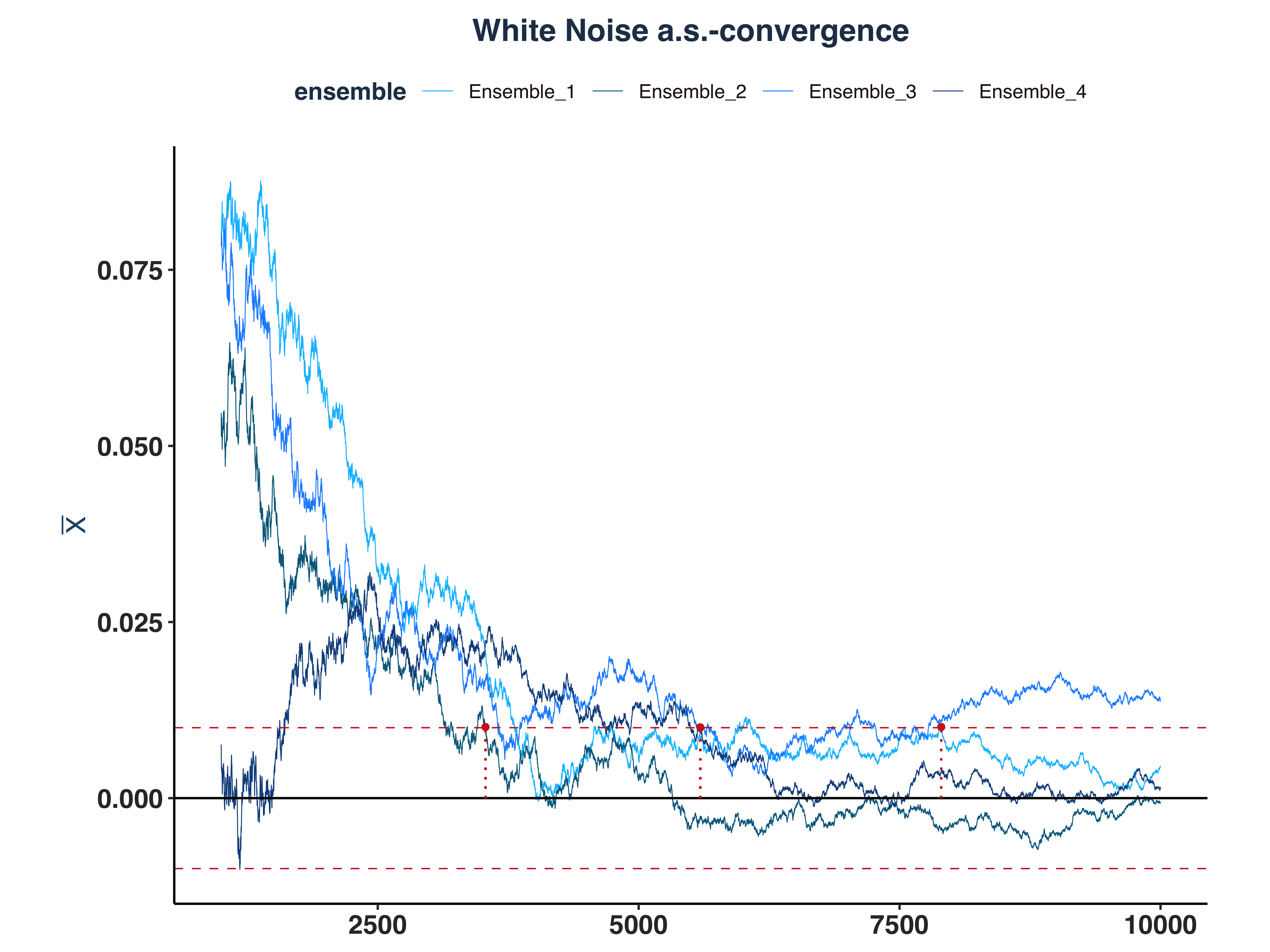

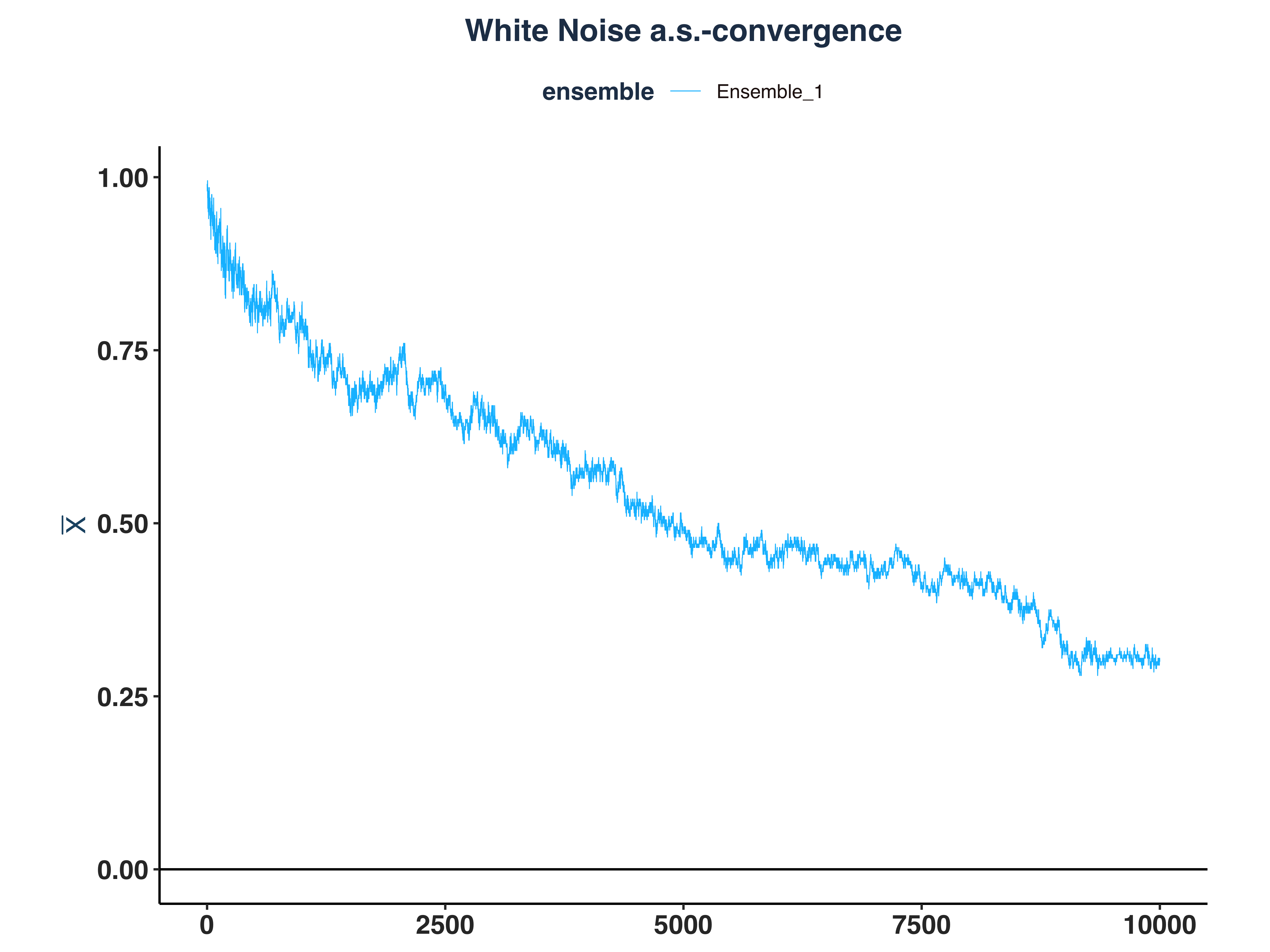

1. White Noise a.s.-convergence

1

2

3

4

5

6

7

8

9

10

11

12

13

|

# Compute \bar{n}(\epsilon, \omega)

n_idx_wn <- apply(abs_dev_wn_dt>eps, 2, \(x) {

rs <- rev(cumsum(rev(as.numeric(x))))

idx <- max(which(rs==1))

`if`(idx == length(x), NULL, idx) # Set to NULL if don't converge

})

# Since the first few hundreds means are so big, I cut them off for better visibility

wn_as_conv_plt <- plot_convergence(mean_wn[1000:10000,], n_idx_wn, "White Noise", "Ensemble_1", eps)

ggsave("Plots/White_Noise_as_convergence.pdf", wn_as_conv_plt,

width = 8, height = 6, dpi = 300)

wn_as_conv_plt

|

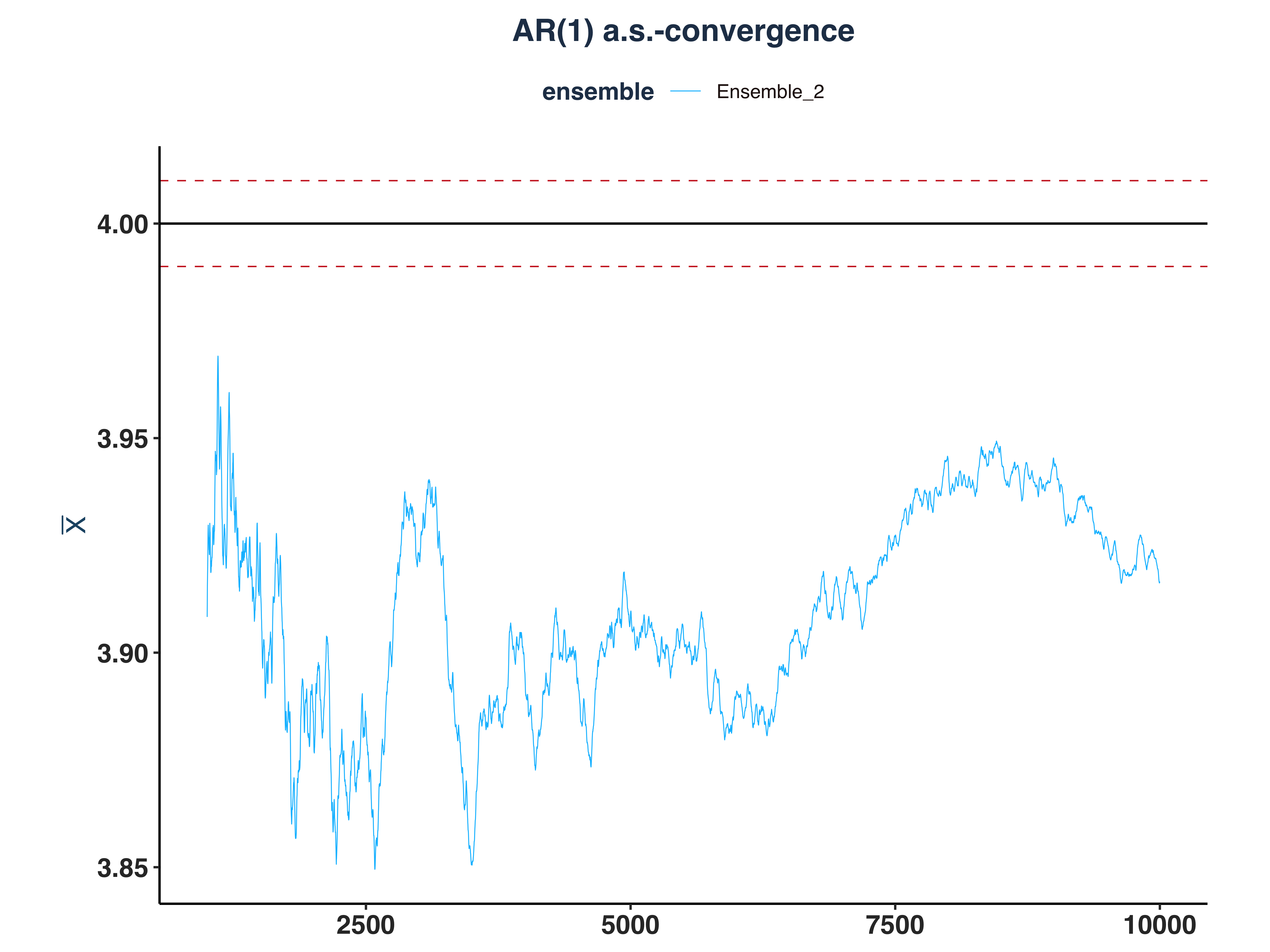

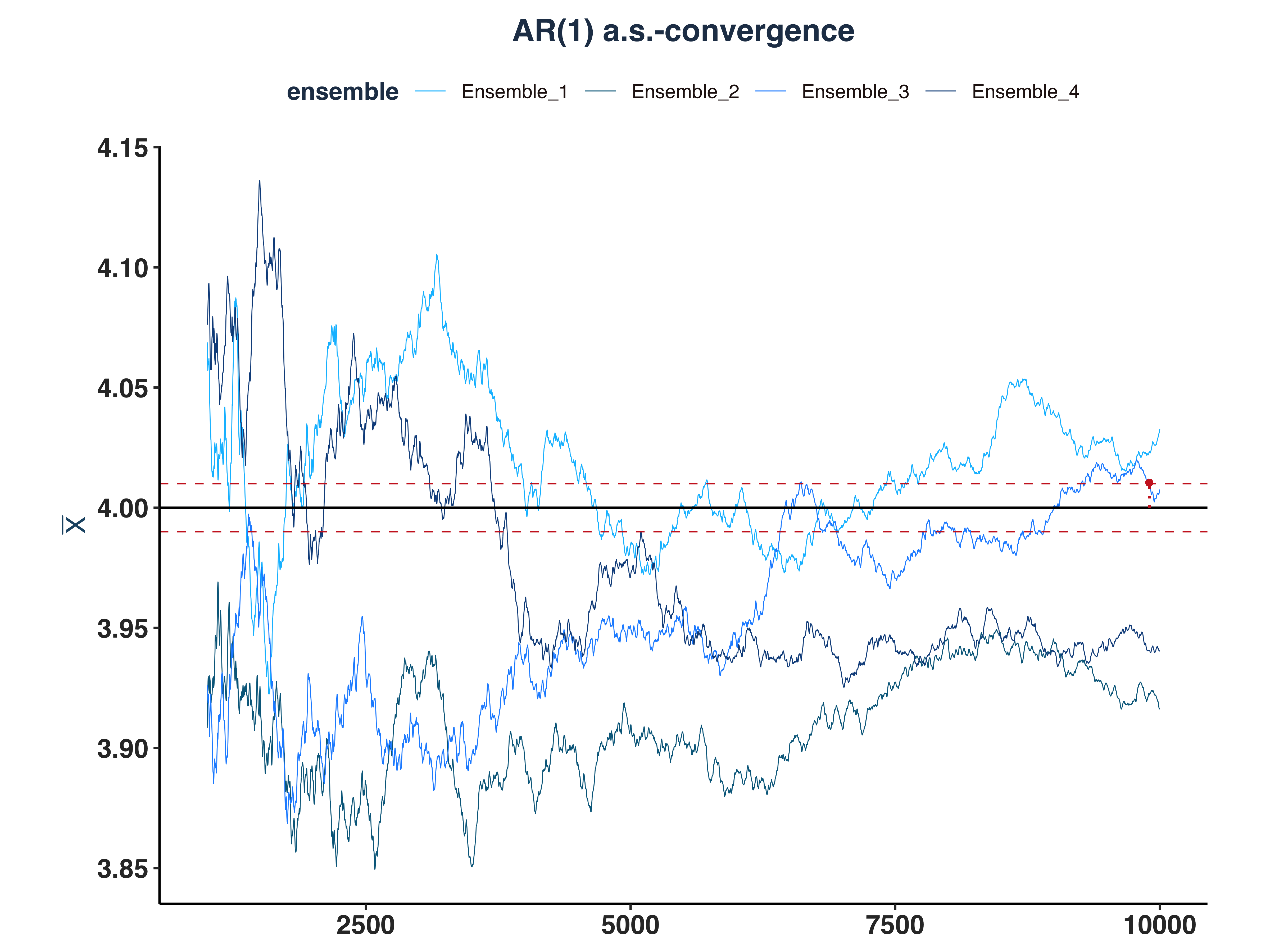

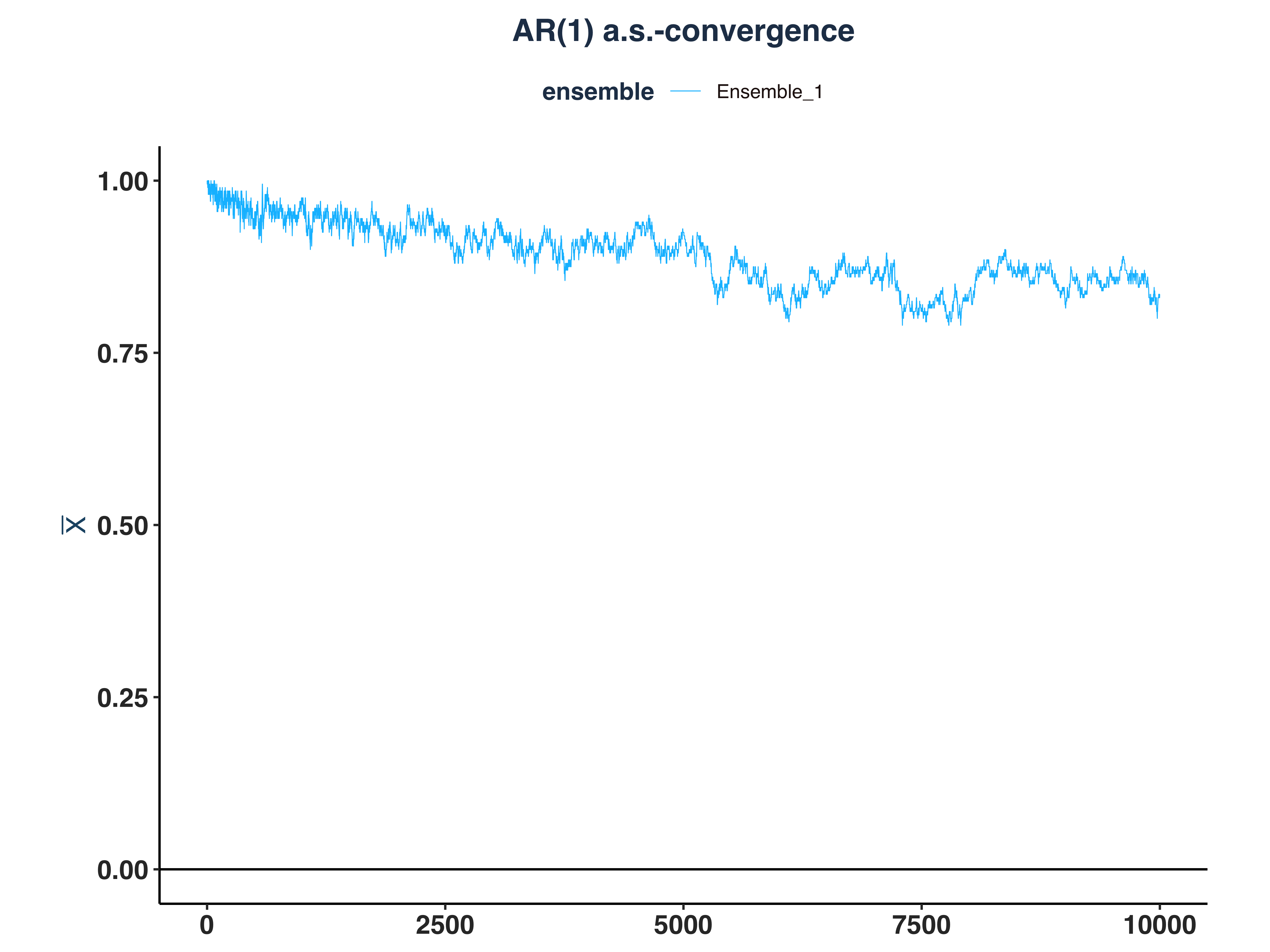

2. AR(1) a.s.-convergence

1

2

3

4

5

6

7

8

9

10

11

12

13

14

|

# Compute \bar{n}(\epsilon, \omega)

n_idx_ar1 <- apply(abs_dev_ar1_dt>eps, 2, \(x) {

rs <- rev(cumsum(rev(as.numeric(x))))

idx <- max(which(rs==1))

`if`(idx == length(x), NULL, idx) # Set to NULL if don't converge

})

# Since the first few hundreds means are so big, I cut them off for better visibility

ar1_as_conv_plt <- plot_convergence(mean_ar1[1000:10000,], n_idx_ar1,

"AR(1)", "Ensemble_2", eps, mu = 4)

ggsave("Plots/AR1_as_convergence.pdf", ar1_as_conv_plt,

width = 8, height = 6, dpi = 300)

ar1_as_conv_plt

|

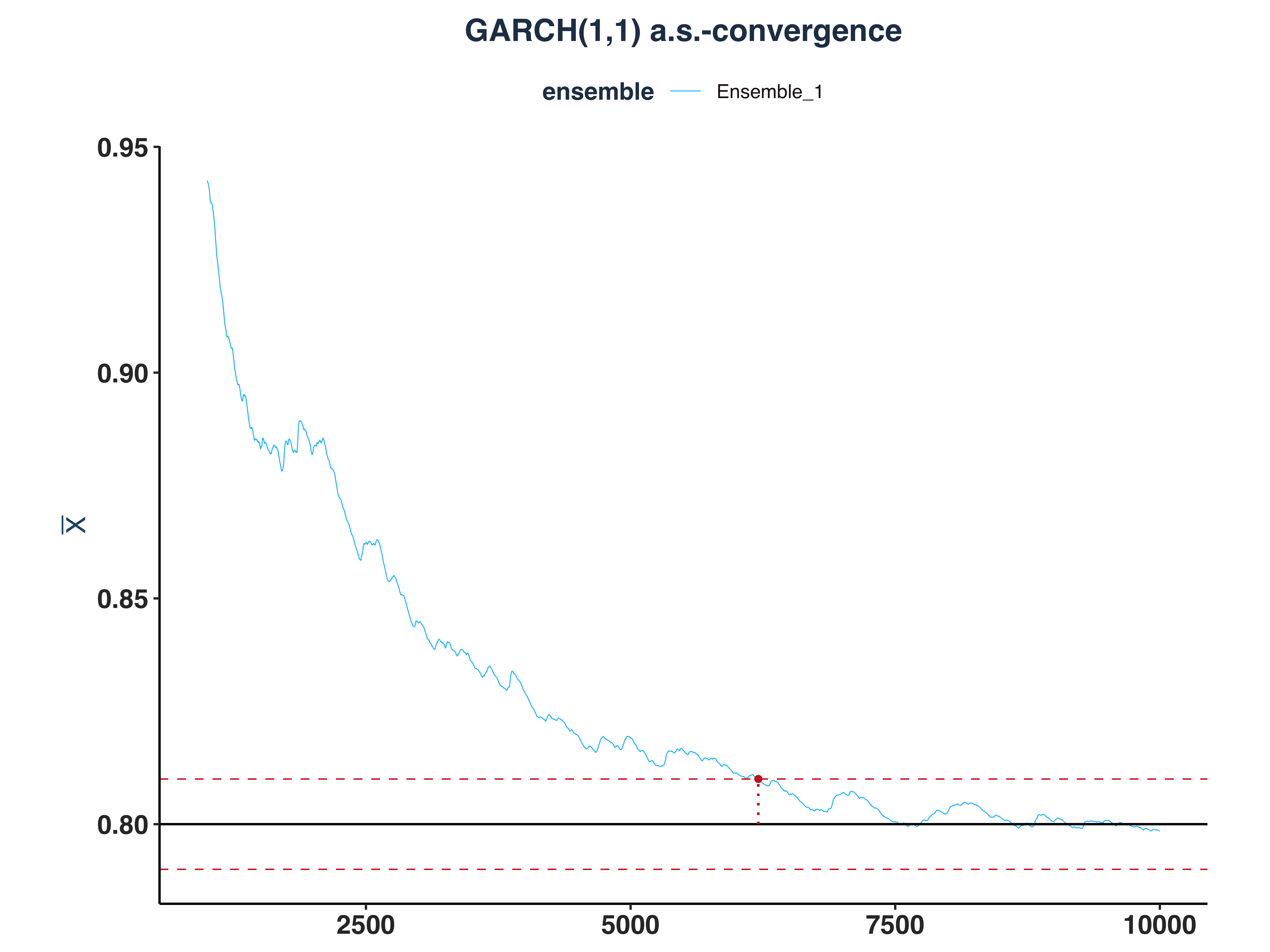

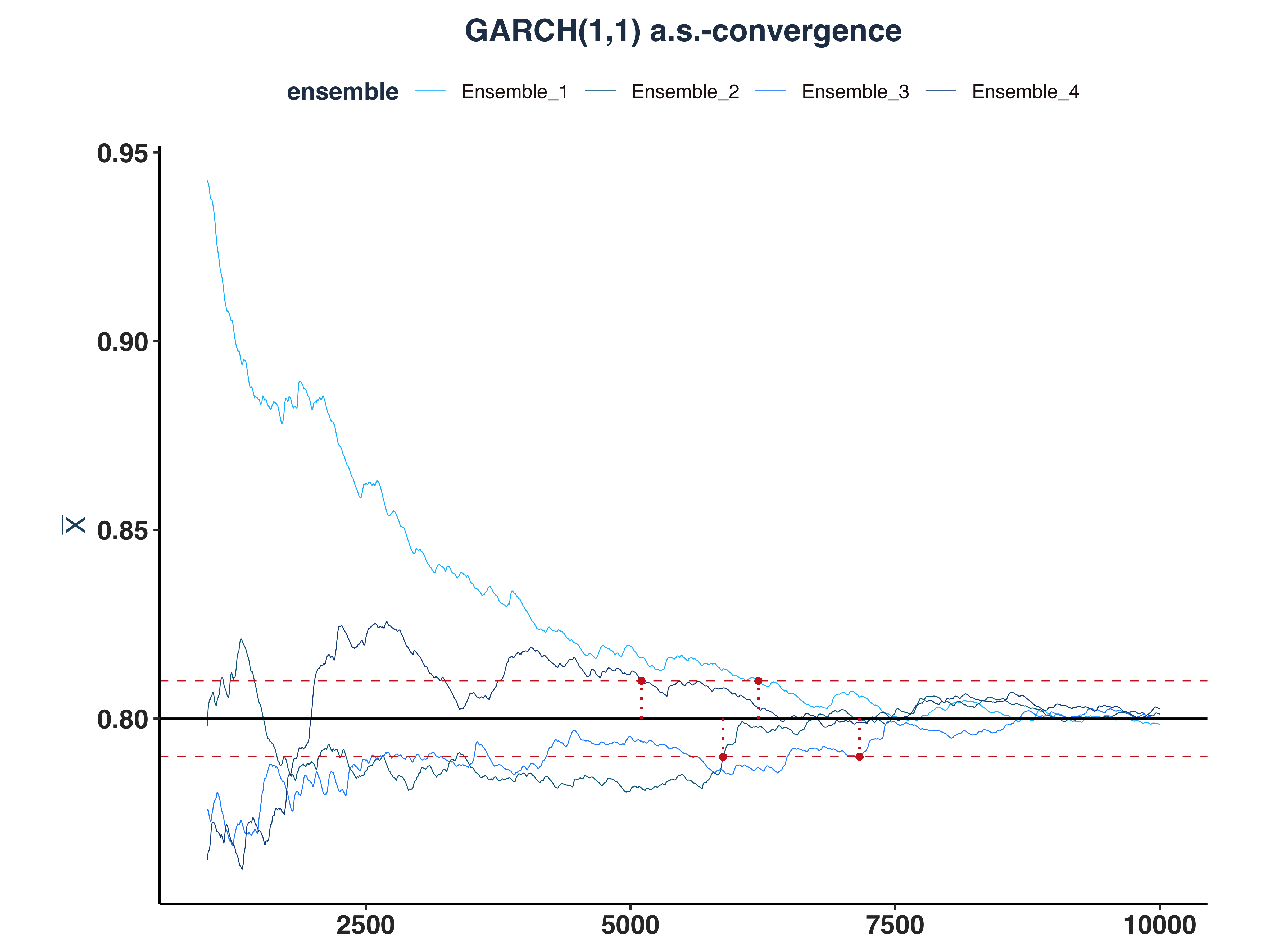

3. GARCH(1,1) a.s.-convergence

1

2

3

4

5

6

7

8

9

10

11

12

13

14

|

# Compute \bar{n}(\epsilon, \omega)

n_idx_g11 <- apply(abs_dev_g11_dt>eps, 2, \(x) {

rs <- rev(cumsum(rev(as.numeric(x))))

idx <- max(which(rs==1))

`if`(idx == length(x), NULL, idx) # Set to NULL if don't converge

})

# Since the first few hundreds means are so big, I cut them off for better visibility

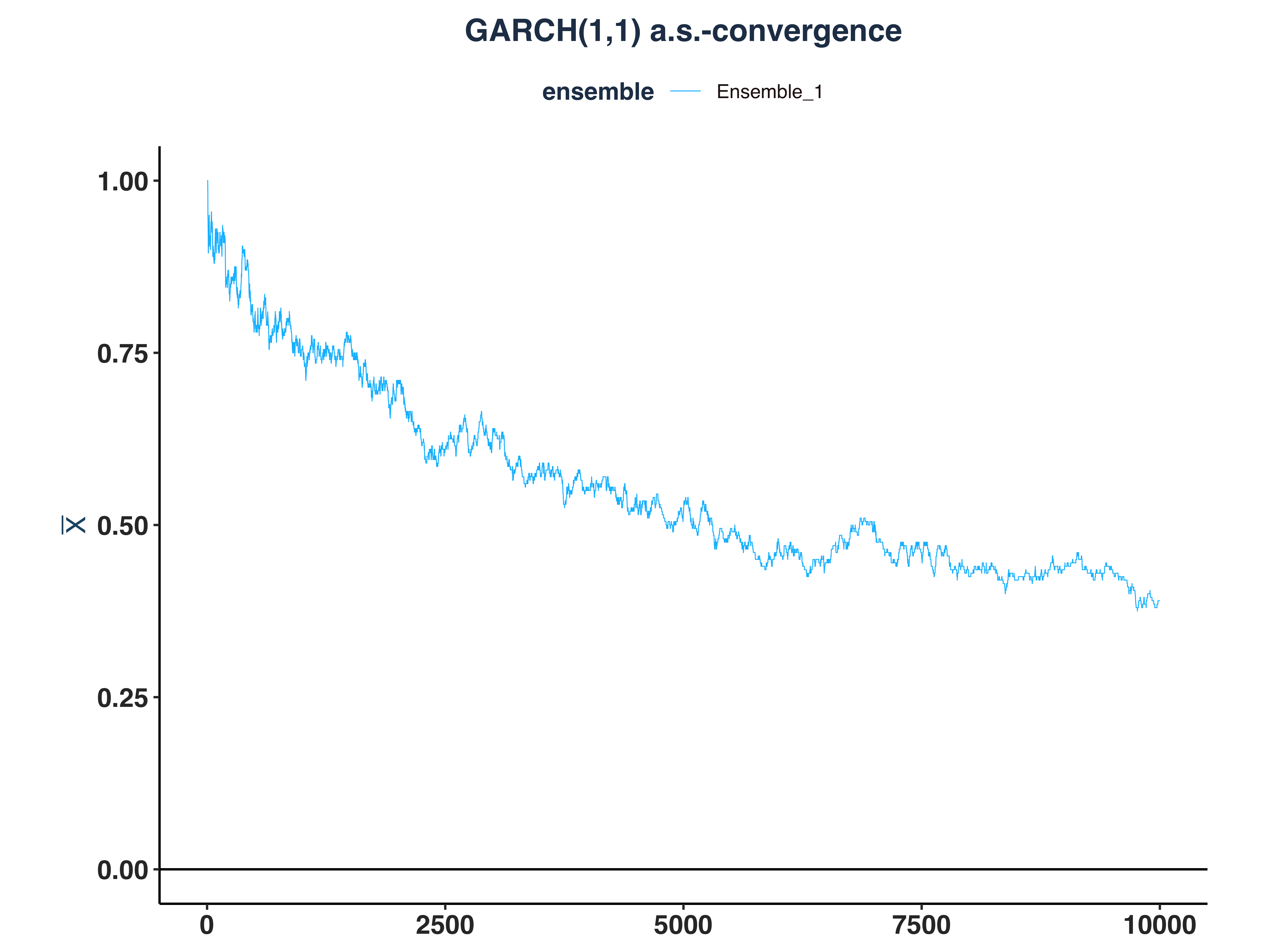

g11_as_conv_plt <- plot_convergence(mean_g11[1000:10000,], n_idx_g11,

"GARCH(1,1)", "Ensemble_1", eps, mu = 0.8)

ggsave("Plots/GARCH11_as_convergence.pdf", g11_as_conv_plt,

width = 8, height = 6, dpi = 300)

g11_as_conv_plt

|

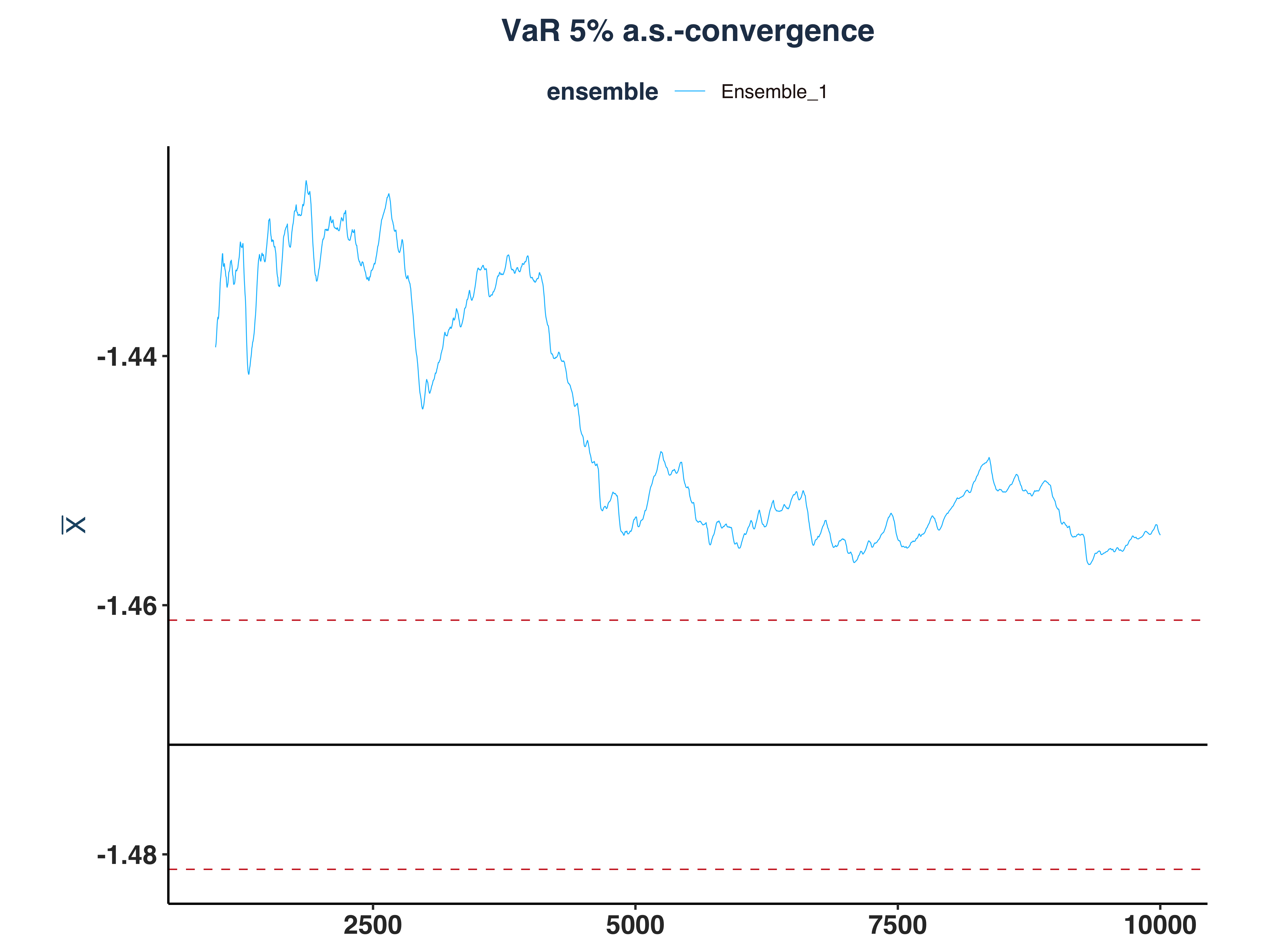

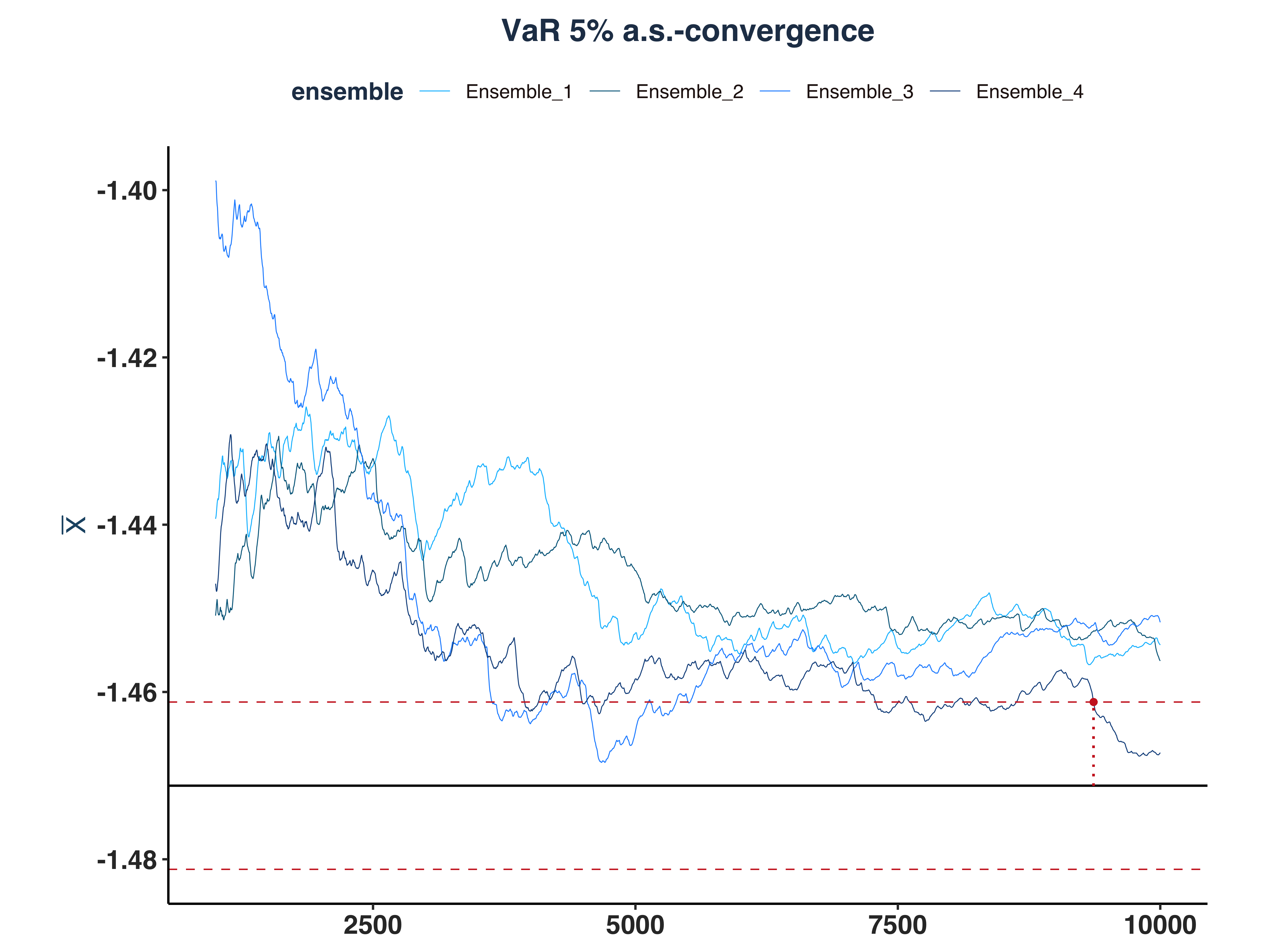

4. VaR 5% a.s.-convergence

1

2

3

4

5

6

7

8

9

10

11

12

13

14

|

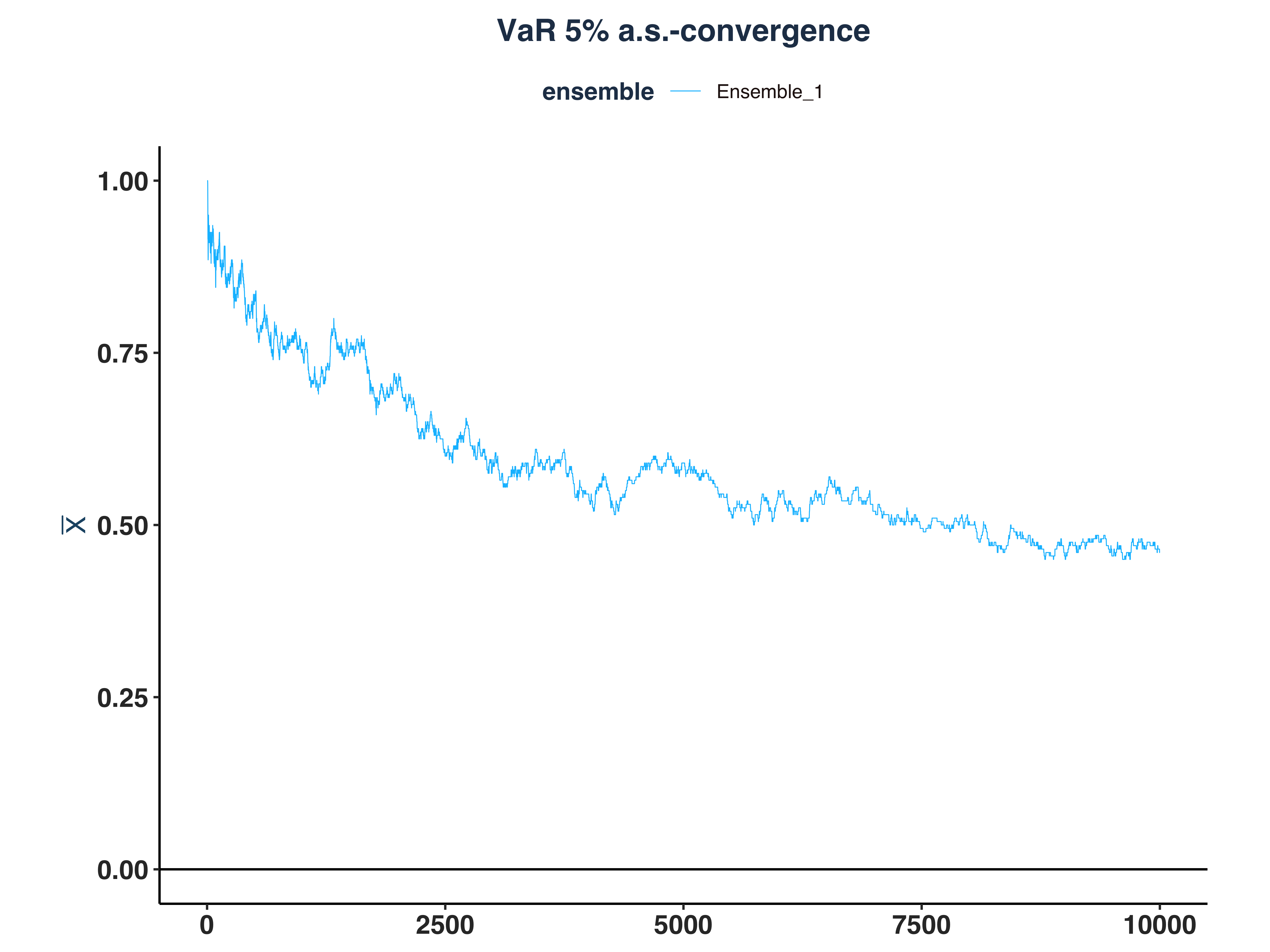

# Compute \bar{n}(\epsilon, \omega)

n_idx_var <- apply(abs_dev_qt_dt>eps, 2, \(x) {

rs <- rev(cumsum(rev(as.numeric(x))))

idx <- max(which(rs==1))

`if`(idx == length(x), NULL, idx) # Set to NULL if don't converge

})

# Since the first few hundreds means are so big, I cut them off for better visibility

var_as_conv_plt <- plot_convergence(mean_qt[1000:10000,], n_idx_var,

"VaR 5%", "Ensemble_1", eps, mu = mu_var)

ggsave("Plots/VaR_5pct_as_convergence.pdf", var_as_conv_plt,

width = 8, height = 6, dpi = 300)

var_as_conv_plt

|

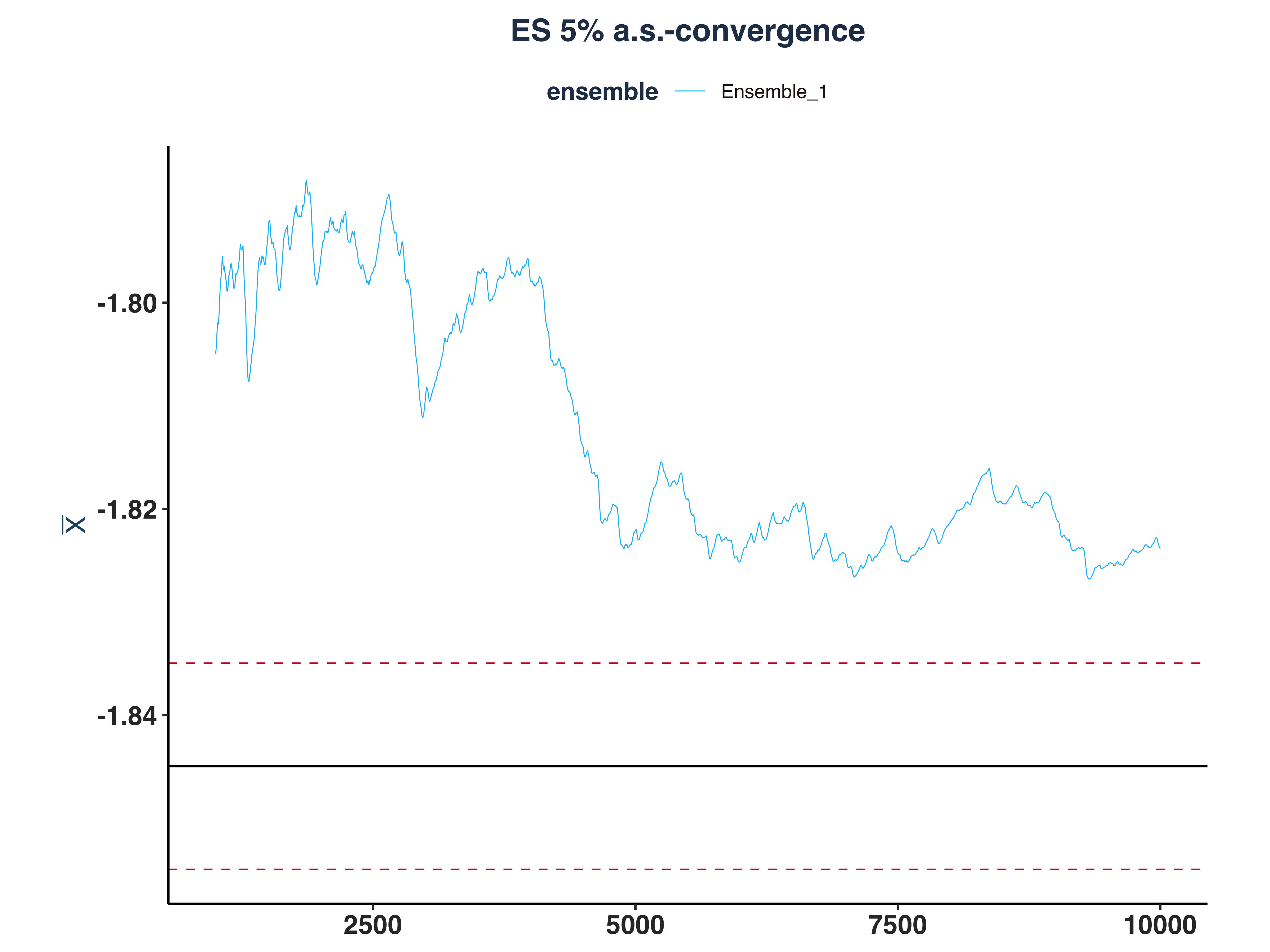

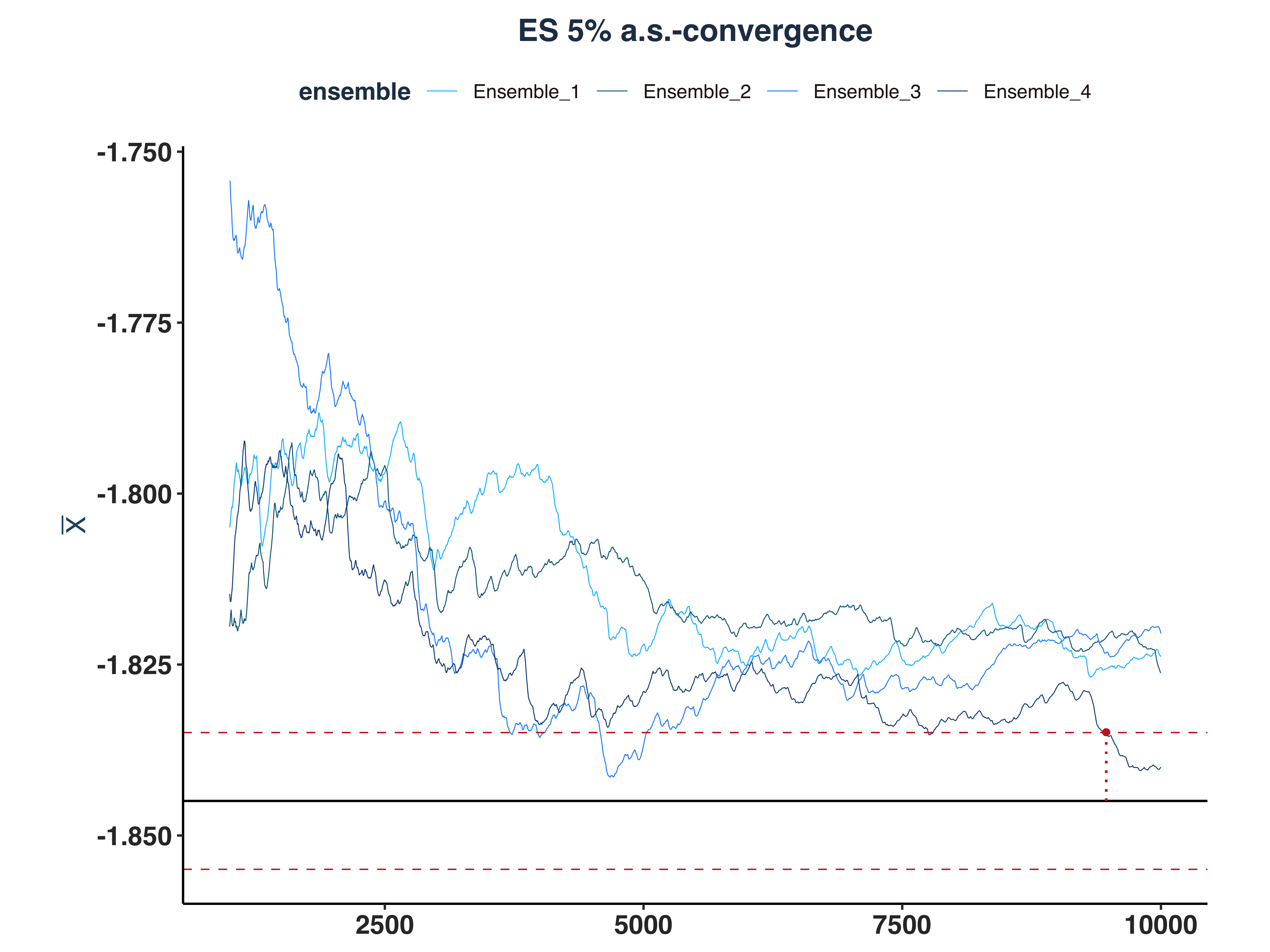

5. ES 5% a.s.-convergence

1

2

3

4

5

6

7

8

9

10

11

12

13

14

|

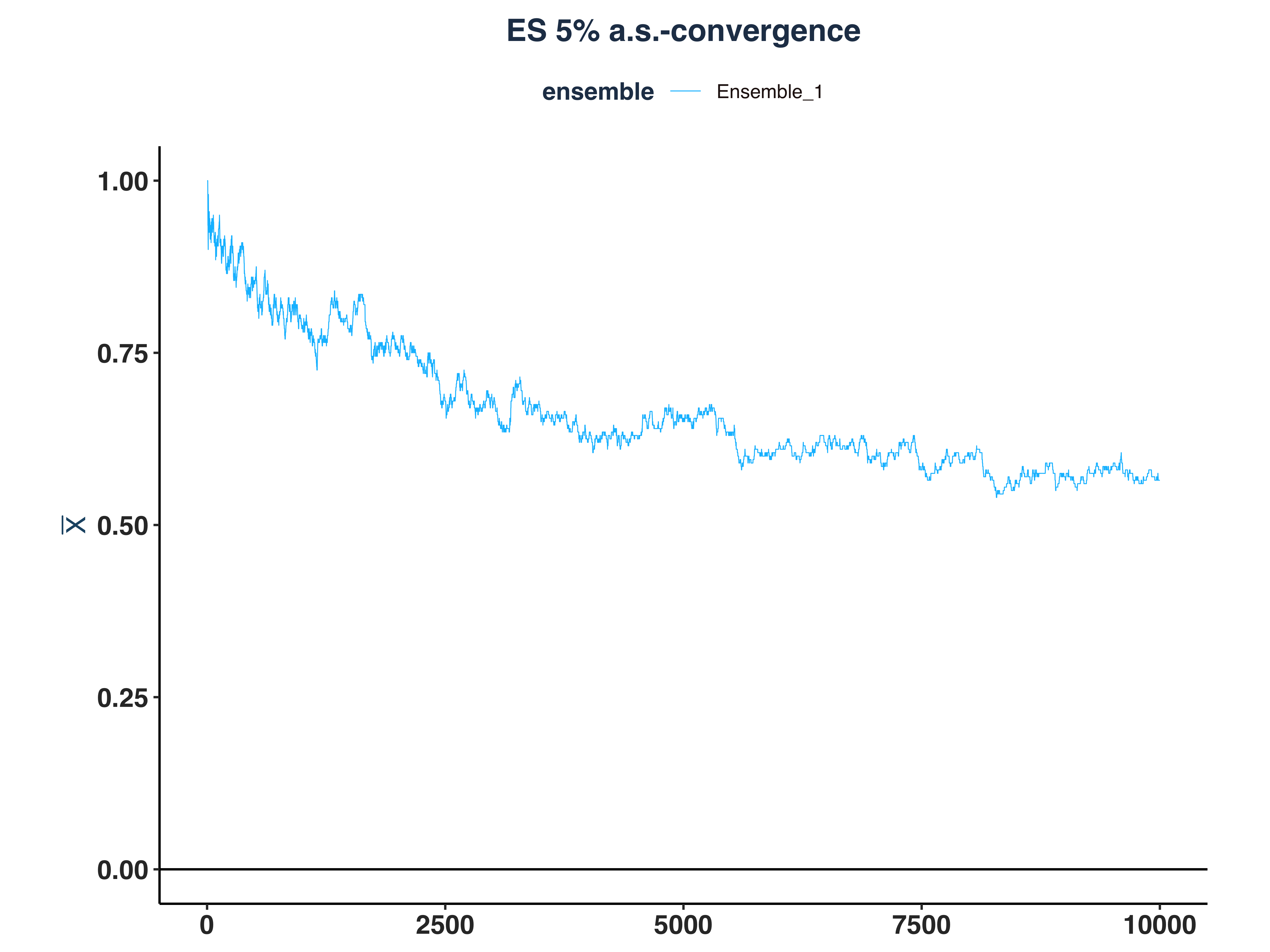

# Compute \bar{n}(\epsilon, \omega)

n_idx_es <- apply(abs_dev_et_dt>eps, 2, \(x) {

rs <- rev(cumsum(rev(as.numeric(x))))

idx <- max(which(rs==1))

`if`(idx == length(x), NULL, idx) # Set to NULL if don't converge

})

# Since the first few hundreds means are so big, I cut them off for better visibility

es_as_conv_plt <- plot_convergence(mean_et[1000:10000,], n_idx_es,

"ES 5%", "Ensemble_1", eps, mu = mu_es)

ggsave("Plots/ES_5pct_as_convergence.pdf", es_as_conv_plt,

width = 8, height = 6, dpi = 300)

es_as_conv_plt

|

iii. Repeat for Four Ensembles#

1. White Noise a.s.-convergence

1

2

3

4

5

6

7

|

# Since the first few hundreds means are so big, I cut them off for better visibility

all_wn_as_conv_plt <- plot_convergence(mean_wn[1000:10000,], n_idx_wn,

"White Noise", "all", eps)

ggsave("Plots/All_White_Noise_as_convergence.pdf", all_wn_as_conv_plt,

width = 8, height = 6, dpi = 300)

all_wn_as_conv_plt

|

As we can see, only 3 ensembles converged.

2. AR(1) a.s.-convergence

1

2

3

4

5

6

7

|

# Since the first few hundreds means are so big, I cut them off for better visibility

all_ar1_as_conv_plt <- plot_convergence(mean_ar1[1000:10000,], n_idx_ar1,

"AR(1)", "all", eps, mu = 4)

ggsave("Plots/All_AR1_as_convergence.pdf", all_ar1_as_conv_plt,

width = 8, height = 6, dpi = 300)

all_ar1_as_conv_plt

|

As we can see, only 1 ensemble converged.

3. GARCH(1,1) a.s.-convergence

1

2

3

4

5

6

7

|

# Since the first few hundreds means are so big, I cut them off for better visibility

all_g11_as_conv_plt <- plot_convergence(mean_g11[1000:10000,], n_idx_g11,

"GARCH(1,1)", "all", eps, mu = 0.8)

ggsave("Plots/All_GARCH11_as_convergence.pdf", all_g11_as_conv_plt,

width = 8, height = 6, dpi = 300)

all_g11_as_conv_plt

|

For GARCH(1,1), all of the realized conditional volatility are a.s.-converged

4. VaR 5% a.s.-convergence

1

2

3

4

5

6

7

|

# Since the first few hundreds means are so big, I cut them off for better visibility

all_var_as_conv_plt <- plot_convergence(mean_qt[1000:10000,], n_idx_var,

"VaR 5%", "all", eps, mu = mu_var)

ggsave("Plots/All_VaR_5pct_as_convergence.pdf", all_var_as_conv_plt,

width = 8, height = 6, dpi = 300)

all_var_as_conv_plt

|

As we can see, only 1 ensemble converged.

5. ES 5% a.s.-convergence

1

2

3

4

5

6

7

|

# Since the first few hundreds means are so big, I cut them off for better visibility

all_es_as_conv_plt <- plot_convergence(mean_et[1000:10000,], n_idx_es,

"ES 5%", "all", eps, mu = mu_es)

ggsave("Plots/All_ES_5pct_as_convergence.pdf", all_es_as_conv_plt,

width = 8, height = 6, dpi = 300)

all_es_as_conv_plt

|

As we can see, only 1 ensemble converged.

f. Convergence in Probability#

i. Simulate Data#

Let’s simulate 200 ensemble and calculate the convergence probabilities accordingly.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

|

# Simulate the time series

set.seed(1340)

T_obs <- 10000

n_ens <- 200

sta_ts_wn <- ARMA.sim(T_obs, 0,0,0, ensembles = n_ens)

sta_ts_ar1 <- ARMA.sim(T_obs, 0.8,0,0.8, ensembles = n_ens)

sta_ts_garch11 <- GARCH.sim(T_obs, 0.04, 0.05, 0.9, ensembles = n_ens)

sta_ts_eq <- VaR.ES.sim(T_obs, 0.05, 0.04, 0.05, 0.9, ensembles = n_ens)

# Compute sequence of averages

mean_wn <- as.data.frame(apply(sta_ts_wn, 2, \(x) cumsum(x)/seq_along(x)))

mean_ar1 <- as.data.frame(apply(sta_ts_ar1, 2, \(x) cumsum(x)/seq_along(x)))

mean_g11 <- as.data.frame(apply(sta_ts_garch11$sigma.2, 2, \(x) cumsum(x)/seq_along(x)))

mean_qt <- as.data.frame(apply(sta_ts_eq$q_t, 2, \(x) cumsum(x)/seq_along(x)))

mean_et <- as.data.frame(apply(sta_ts_eq$e_t, 2, \(x) cumsum(x)/seq_along(x)))

# Compute p_T

eps <- 0.01

mu_var <- sqrt(0.8)*qnorm(0.05, 0, 1)

mu_es <- sqrt(0.8)*(-dnorm(qnorm(0.05, 0, 1), 0, 1) / 0.05)

prob_dev_wn_dt <- apply(abs(mean_wn-0), 1, \(x) {mean(x>eps)})

prob_dev_ar1_dt <- apply(abs(mean_ar1-4), 1, \(x) {mean(x>eps)})

prob_dev_g11_dt <- apply(abs(mean_g11-0.8), 1, \(x) {mean(x>eps)})

prob_dev_qt_dt <- apply(abs(mean_qt-mu_var), 1, \(x) {mean(x>eps)})

prob_dev_et_dt <- apply(abs(mean_et-mu_es), 1, \(x) {mean(x>eps)})

# Set names

list2env(lapply(mget(c("prob_dev_wn_dt", "prob_dev_ar1_dt", "prob_dev_g11_dt",

"prob_dev_qt_dt", "prob_dev_et_dt")),

\(x) setNames(x, "Ensemble_1")), envir = .GlobalEnv)

|

1

|

## <environment: R_GlobalEnv>

|

1

2

3

4

5

|

# Create plot data

list2env(lapply(mget(c("prob_dev_wn_dt", "prob_dev_ar1_dt", "prob_dev_g11_dt",

"prob_dev_qt_dt", "prob_dev_et_dt")),

\(x) data.frame(Index = seq_len(T_obs), Ensemble_1 = x)),

envir = .GlobalEnv)

|

1

|

## <environment: R_GlobalEnv>

|

1

2

|

# Print out a series to double-check

tail(prob_dev_g11_dt,10)

|

1

2

3

4

5

6

7

8

9

10

11

|

## Index Ensemble_1

## 9991 9991 0.39

## 9992 9992 0.39

## 9993 9993 0.39

## 9994 9994 0.39

## 9995 9995 0.39

## 9996 9996 0.39

## 9997 9997 0.39

## 9998 9998 0.39

## 9999 9999 0.39

## 10000 10000 0.39

|

ii. Plot the Convergence in Probability#

1. White Noise Kernel Density

1

2

3

4

5

6

|

wn_ip_conv_plt <- plot_convergence(prob_dev_wn_dt, NULL, "White Noise", "Ensemble_1",

eps = 0, mu = 0) # (eps,mu)=(0,0) values a specifically for in probability convergence

ggsave("Plots/White_Noise_ip_convergence.pdf", wn_ip_conv_plt,

width = 8, height = 6, dpi = 300)

wn_ip_conv_plt

|

2. AR(1) Kernel Density

1

2

3

4

5

6

|

ar1_ip_conv_plt <- plot_convergence(prob_dev_ar1_dt, NULL, "AR(1)", "Ensemble_1",

eps=0, mu = 0)

ggsave("Plots/AR1_ip_convergence.pdf", ar1_ip_conv_plt,

width = 8, height = 6, dpi = 300)

ar1_ip_conv_plt

|

3. GARCH(1,1) Kernel Density

1

2

3

4

5

6

|

g11_ip_conv_plt <- plot_convergence(prob_dev_g11_dt, NULL, "GARCH(1,1)",

"Ensemble_1", eps = 0, mu = 0)

ggsave("Plots/GARCH11_ip_convergence.pdf", g11_ip_conv_plt,

width = 8, height = 6, dpi = 300)

g11_ip_conv_plt

|

4. VaR 5% Kernel Density

1

2

3

4

5

6

|

var_ip_conv_plt <- plot_convergence(prob_dev_qt_dt, NULL, "VaR 5%", "Ensemble_1",

eps = 0, mu = 0)

ggsave("Plots/VaR_5pct_ip_convergence.pdf", var_ip_conv_plt,

width = 8, height = 6, dpi = 300)

var_ip_conv_plt

|

5. ES 5% Kernel Density

1

2

3

4

5

6

|

es_ip_conv_plt <- plot_convergence(prob_dev_et_dt, NULL, "ES 5%", "Ensemble_1",

eps = 0, mu = 0)

ggsave("Plots/ES_5pct_ip_convergence.pdf", es_ip_conv_plt,

width = 8, height = 6, dpi = 300)

es_ip_conv_plt

|

g. Simulate 200 Ensembles and Find \(\bar{n}(\varepsilon=0.01, \omega)\)#

i. Simulate and Compute \(\bar{n}\)#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

|

# Define file paths

data_files <- list(

wn = "Data/sta_ts_wn_dt.rds",

ar1 = "Data/sta_ts_ar1_dt.rds",

garch11 = "Data/sta_ts_garch11_dt.rds",

qt = "Data/sta_ts_qt_dt.rds",

et = "Data/sta_ts_et_dt.rds"

)

# Check if all files exist

all_files_exist <- all(sapply(data_files, file.exists))

if (!all_files_exist) {

# Simulate the time series

set.seed(1340)

T_obs <- 100000

n_ens <- 200

sta_ts_wn <- ARMA.sim(T_obs, 0,0,0, ensembles = n_ens)

sta_ts_ar1 <- ARMA.sim(T_obs, 0.8,0,0.8, ensembles = n_ens)

sta_ts_garch11 <- GARCH.sim(T_obs, 0.04, 0.05, 0.9, ensembles = n_ens)

sta_ts_eq <- VaR.ES.sim(T_obs, 0.05, 0.04, 0.05, 0.9, ensembles = n_ens)

# Convert simulated data to data.table

sta_ts_wn_dt <- as.data.table(sta_ts_wn)

sta_ts_ar1_dt <- as.data.table(sta_ts_ar1)

sta_ts_garch11_dt <- as.data.table(sta_ts_garch11$sigma.2)

sta_ts_qt_dt <- as.data.table(sta_ts_eq$q_t)

sta_ts_et_dt <- as.data.table(sta_ts_eq$e_t)

# Set column names

col_names <- paste0("Ensemble_", 1:n_ens)

setnames(sta_ts_wn_dt, col_names)

setnames(sta_ts_ar1_dt, col_names)

setnames(sta_ts_garch11_dt, col_names)

setnames(sta_ts_qt_dt, col_names)

setnames(sta_ts_et_dt, col_names)

# Save datasets to disk

saveRDS(sta_ts_wn_dt, file = data_files$wn)

saveRDS(sta_ts_ar1_dt, file = data_files$ar1)

saveRDS(sta_ts_garch11_dt, file = data_files$garch11)

saveRDS(sta_ts_qt_dt, file = data_files$qt)

saveRDS(sta_ts_et_dt, file = data_files$et)

} else {

# Load saved datasets

sta_ts_wn_dt <- readRDS(data_files$wn)

sta_ts_ar1_dt <- readRDS(data_files$ar1)

sta_ts_garch11_dt <- readRDS(data_files$garch11)

sta_ts_qt_dt <- readRDS(data_files$qt)

sta_ts_et_dt <- readRDS(data_files$et)

}

# Compute sequence of averages using data.table syntax

# apply to all column, please advise https://cran.r-project.org/web/packages/data.table/vignettes/datatable-sd-usage.html

mean_wn <- sta_ts_wn_dt[, lapply(.SD, \(x) cumsum(x)/seq_along(x))]

mean_ar1 <- sta_ts_ar1_dt[, lapply(.SD, \(x) cumsum(x)/seq_along(x))]

mean_g11 <- sta_ts_garch11_dt[, lapply(.SD, \(x) cumsum(x)/seq_along(x))]

mean_qt <- sta_ts_qt_dt[, lapply(.SD, \(x) cumsum(x)/seq_along(x))]

mean_et <- sta_ts_et_dt[, lapply(.SD, \(x) cumsum(x)/seq_along(x))]

|

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

|

# Compute deviations

eps <- 0.01

mu_var <- sqrt(0.8)*qnorm(0.05, 0, 1)

mu_es <- sqrt(0.8)*(-dnorm(qnorm(0.05, 0, 1), 0, 1) / 0.05)

abs_dev_wn_dt <- mean_wn[, lapply(.SD, \(x) abs(x - 0))] # mu=0

abs_dev_ar1_dt <- mean_ar1[, lapply(.SD, \(x) abs(x - 4))] # mu=4

abs_dev_g11_dt <- mean_g11[, lapply(.SD, \(x) abs(x - 0.8))] # mu=0.8

abs_dev_qt_dt <- mean_qt[, lapply(.SD, \(x) abs(x - mu_var))] # mu=-1.4712

abs_dev_et_dt <- mean_et[, lapply(.SD, \(x) abs(x - mu_es))] # mu=-1.8449

# Add Index column for plotting

mean_wn[, Index := .I]

mean_ar1[, Index := .I]

mean_g11[, Index := .I]

mean_qt[, Index := .I]

mean_et[, Index := .I]

# Reorder columns to put Index first

col_names <- paste0("Ensemble_", 1:ncol(sta_ts_wn_dt))

setcolorder(mean_wn, c("Index", col_names))

setcolorder(mean_ar1, c("Index", col_names))

setcolorder(mean_g11, c("Index", col_names))

setcolorder(mean_qt, c("Index", col_names))

setcolorder(mean_et, c("Index", col_names))

|

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

|

# Create a single list containing all data

sta_ts_all_dt <- list(

wn = abs_dev_wn_dt,

ar1 = abs_dev_ar1_dt,

g11 = abs_dev_g11_dt,

qt = abs_dev_qt_dt,

et = abs_dev_et_dt

)

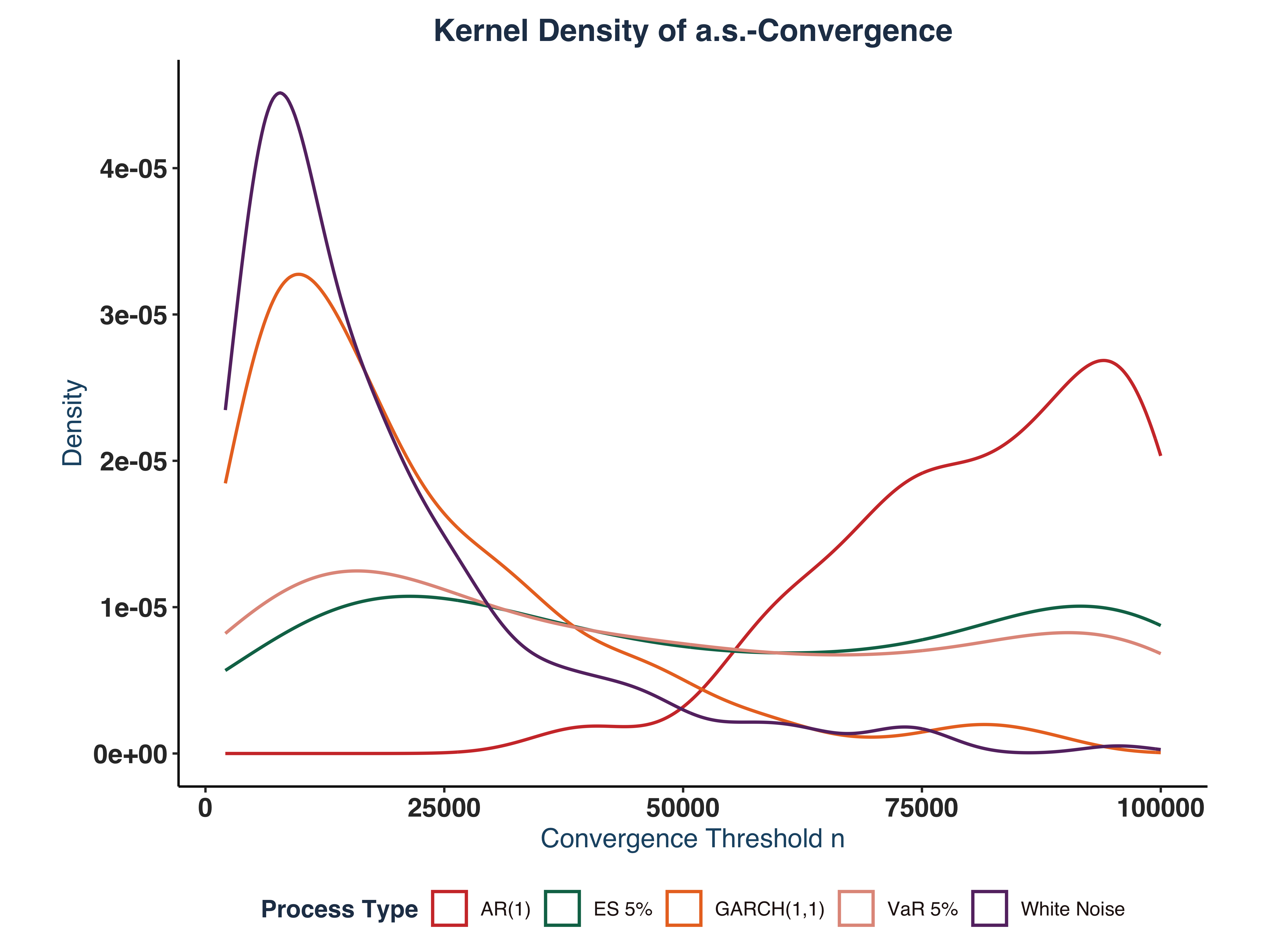

n_idx_ls <- lapply(sta_ts_all_dt, \(dt) {

dt[, lapply(.SD, \(x) {

rs <- rev(cumsum(rev(as.numeric(x > eps))))

idx <- max(which(rs == 1))

if(idx == length(x)) NA_integer_ else idx

})]

})

# Check convergence

n_non_conv <- sapply(n_idx_ls, \(dt) dt[, sum(sapply(.SD, is.na))])

if(sum(n_non_conv) > 0) {

cat("Non-converged ensembles exist")

} else {

cat("All ensembles converged")

}

|

1

|

## Non-converged ensembles exist

|

1

2

3

4

5

6

|

data.table(

Series = names(n_non_conv),

Non_Converged = as.numeric(n_non_conv),

Total_Ensembles = sapply(n_idx_ls, ncol),

Convergence_Rate = round((1 - as.numeric(n_non_conv) / sapply(n_idx_ls, ncol)) * 100, 2)

)

|

1

2

3

4

5

6

7

|

## Series Non_Converged Total_Ensembles Convergence_Rate

## <char> <num> <int> <num>

## 1: wn 0 200 100

## 2: ar1 118 200 41

## 3: g11 2 200 99

## 4: qt 76 200 62

## 5: et 126 200 37

|

ii. Plot Kernel Density#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

|

# Create a mapping for proper names

process_names <- c("wn" = "White Noise", "ar1" = "AR(1)", "g11" = "GARCH(1,1)",

"qt" = "VaR 5%", "et" = "ES 5%")

# Combine all series

plt_dt <- rbindlist(lapply(names(n_idx_ls), \(name) {

data.table(n = as.vector(t(n_idx_ls[[name]])),

process = process_names[name])

}))

# Create the plot with proper labels

ts_colors <- c("White Noise" = "#663171FF",

"AR(1)" = "#CF3A36FF",

"GARCH(1,1)" = "#EA7428FF",

"VaR 5%" = "#E2998AFF",

"ES 5%" = "#0C7156FF")

dens_plt <- ggplot(plt_dt, aes(x = n)) +

geom_density(aes(color = process), linewidth = 0.7) +

scale_fill_manual(values = ts_colors)+

scale_color_manual(values = ts_colors)+

theme(panel.grid.major = element_blank(),

panel.grid.minor = element_blank(),

panel.border = element_blank(),

panel.background = element_blank(),

legend.position = "bottom") +

global_fonts+

labs(title = "Kernel Density of a.s.-Convergence",

x = "Convergence Threshold n",

y = "Density",

color = "Process Type")

ggsave("Plots/Convergence_kernel_density.pdf", dens_plt,

width = 8, height = 6, dpi = 300)

dens_plt

|

Exercise 3 - Forecasting Exercise#

a. Pseudo-out-of Sample One-step Ahead Forecast#

i. Setup Forecast#

First, we split the Coca-Cola (KO) stock log returns into two datasets: train_dt (70%) and test_dt (30%).

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

|

# Model Setup ----

# 1. Crawl More data

if (!file.exists("Data/ex3_price_dt.rds")) {

# Download Data

ex3_pr_dt <- tq_get("KO",get = "stock.prices", from = "1990-01-01", to = "2025-08-09")

# Save model data

saveRDS(ex3_pr_dt, file = "Data/ex3_price_dt.rds")

} else {

# Access saved stock data

ex3_pr_dt <- readRDS("Data/ex3_price_dt.rds")

}

# Prepare return data

ex3_ret_dt <- prep_return_dt(ex3_pr_dt)

# Extract different frequencies

ex3_daily_dt <- ex3_ret_dt$daily

# 2. Train Test split

ex3_daily_dt <- data.table(ex3_daily_dt)

n_obs <- nrow(ex3_daily_dt)

train_idx <- 1:floor(n_obs*0.7)

train_dt <- ex3_daily_dt[train_idx, c("date","logret")]

test_dt <- ex3_daily_dt[!train_idx, c("date","logret")]

# 2. Config

control.solnp <- list(rho = 1,

outer.iter = 600,

inner.iter = 800,

delta = 1e-7,

tol = 1e-6)

# Print out lengths

sprintf("Number of observation in Train Dataset: %d", nrow(train_dt))

|

1

|

## [1] "Number of observation in Train Dataset: 6276"

|

1

|

sprintf("Number of observation in Test Dataset: %d", nrow(test_dt))

|

1

|

## [1] "Number of observation in Test Dataset: 2690"

|

ii. Model Selection#

Based on the results from Exercise 1.b, we observe that GARCH(1,1) is the best candidate for our problem. Following previouse researches of Nkrumah, M. A. (2025), Enkhtur, A. (2022), Yatawara, K. C. M. R. A. B. (2023), Sjöholm, S. (2015), and So, M. K. P., Chu, A. M. Y., Lo, C. C. Y., & Ip, C. Y. (2021), we will compare the performance among three models: GJR-GARCH-N, EGARCH, and GARCH-t.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

|

# Get bounds

mdl_name <- "GJR-GARCH-N"

bounds <- get_garch_bounds(mdl_name, c(1,1))

if (!file.exists("Data/ex3_gjrgn_mdl.rds")) {

# Estimate GJR-GARCH-N

ex3_gjr_mdl <- estimate_garch_dynamic(

y = train_dt[["logret"]],

n_starts = 20,

garch_order = c(1,1),

model_type = "GJR-GARCH-N",

distribution = "norm",

lower_bounds = bounds$lower, upper_bounds = bounds$upper,

loglik_func = Likelihood.GARCH,

ineq_constraints = Inequality.constraints.GARCH,

custom_control = control.solnp

)

# Save results

saveRDS(ex3_gjr_mdl, file = "Data/ex3_gjrgn_mdl.rds")

} else {

# Access saved data

ex3_gjr_mdl <- readRDS("Data/ex3_gjrgn_mdl.rds")

}

# Check best log-likelihood

# sprintf("Best LLH rugarch %s: %.2f", mdl_name, ex3_gjr_mdl$best_estimates$rugarch["LogL"])

|

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

|

# Get bounds

mdl_name2 <- "EGARCH"

bounds2 <- get_garch_bounds(mdl_name2, c(1,1))

if (!file.exists("Data/ex3_eg_mdl.rds")) {

# Estimate GJR-GARCH-N

ex3_eg_mdl <- estimate_garch_dynamic(

y = train_dt[["logret"]],

n_starts = 20,

garch_order = c(1,1),

model_type = mdl_name2,